Largely unloved until recent years, cobalt is welcoming a new era of soaring demand, sparked by the metal’s uptake in the surging lithium-ion battery sector, with a rush of ASX-listed mineral stocks pegging up cobalt ground to take advantage of this new market.

Powering the lithium-ion battery’s demand is the flourishing sustainable energy and electric vehicle markets.

Transparency Market Research predicts the lithium-ion battery market will be valued at US$77.4 billion by 2024, primarily driven by electric vehicles.

Until the advent of the lithium-ion battery, cobalt was traditionally a by-product of nickel, silver, copper, lead, and iron mining.

Now, the metal is sought in its own right for incorporation in the lithium-ion battery, which actually contains more cobalt than lithium.

Lithium-ion battery

For those unfamiliar with the lithium-ion battery, it has three primary components: anode, cathode, and the electrolyte which is made from lithium.

The anode is graphite, and the cathode is a combination of several formulations but mostly includes cobalt or variations of cobalt, nickel and manganese.

Cobalt is now deemed a critical mineral, with more than 45% of the metal directed to the battery market.

Cobalt history and other uses

Throughout the centuries, cobalt was traditionally used as a colour additive in porcelain, glass, pottery, tiles and enamel.

By 1735, a Swedish scientist isolated the mineral and its use as a metal stems from Elwood Haynes’ work in the early 1900s.

Other end uses include incorporation in corrosion resistant applications as well as alloys for some stainless steels, jet engines, magnets, and gas turbines.

Market dynamics

The majority of the world’s cobalt arises out of the Democratic Republic of Congo (DRC). According to the US Geological Survey, the DRC contributed 66,000t to global cobalt supplies in 2016, which is more than half the world’s 123,000t produced that year.

This poses its own set of ethical and supply challenges, with a black cloud hanging over the country due to its prolific use of child labour and ongoing leadership instability.

Eurasian Resources Group Tony Southgate told people attending a recent seminar it was “inevitable” many people there had a smart device in their pocket or bag that comprised cobalt derived from child labour.

As downstream users such as Tesla and Apple seek more ethically sourced cobalt, this opens the door for the rest of the world to ramp up cobalt operations to meet the supply gap and offer a more ethical and stable origin.

Adding to the situation, is increasing cobalt demand, which is forecast to swell from about 53,000t in 2015 to 120,000 by 2025.

Outside of the DRC, smaller cobalt operations can be found across China, Canada, Russia, Australia, Zambia, the Philippines, Cuba, Madagascar, New Caledonia and South Africa.

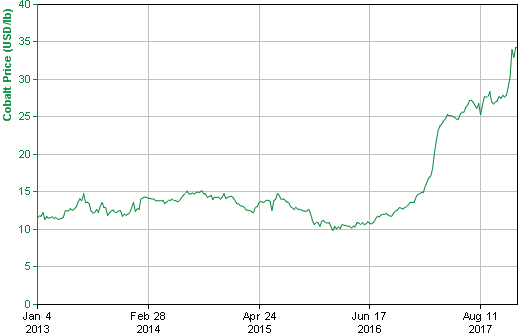

Cobalt price

In the past month, the market has watched the cobalt price smash through the US$70,000 per tonne ceiling, which it has been unable to negate for the past decade when it achieved its pre-global financial crisis peak above US$110,000/t, before sliding to below US$30,000/t in 2013 and again in early 2016.

The metal began its reascent during 2016, and by early December 2017, cobalt has surged almost overnight to hit US$75,000/t on 8 December. At the time of writing, the cobalt price has hovered about US$75,500 per tonne since late December.

Due to recent price hikes and supply bottlenecks, many ASX-listed small cap explorers are now actively reviewing their current projects with numerous companies reporting substantial cobalt mineralisation discoveries in old and new drill samples at their Australian projects and abroad.

Cobalt stocks on the ASX

As the cobalt price appears on the climb back to its former glory, we’ve taken a look at the ASX-listed stocks with exposure to the commodity.

Aeon Metals (ASX: AML)

In Australia, Aeon Metals recently announced its highest cobalt and copper grades ever from the PY3 prospect, which is part of its flagship wholly-owned Walford Creek project in Queensland.

The final two holes of the company’s 2017 phase two drilling campaign intersected wide cobalt mineralisation grading up to 0.44%.

Walford has a current resource of 73.3 million tonnes grading 0.08% cobalt, equating to about 60,000t of the mineral.

The company is finalising a resource upgrade which is due out by the end of the month or early January and its next step will be to carry out a feasibility study and investigate roasting to enhance recoveries.

According to Aeon Metals, Walford Creek hosts one of Australia’s “most advanced cobalt sulphide deposits” and estimates the cobalt value within the project at A$4.4 billion.

On 12 December, Aeon reported it had received a total of $185,000 in government funding, which will cover 50% of a planned seismic and drilling activity. A few days later the company announced it had raised A$30 million to fund an expanded 2018 drilling program and a widen the scope of its bankable feasibility study.

Anson Resources (ASX: ASN)

Although focussed on developing its Paradox lithium brine project in the US, Anson Resources tenement applications over the Hooley Wells nickel, cobalt project 300km east of Geraldton in WA.

Previous exploration at the project has returned 22m grading 0.061% cobalt and 0.97% nickel from near surface including a 4m interval grading 0.11% cobalt and 1.4% nickel.

The tenements are anticipated to be granted shortly, with exploration to begin soon after.

Archer Exploration (ASX: AXE)

Over at Archer Exploration, the company announced on 6 December, it had uncovered cobalt grading up to 0.52% from rock chip sampling at its Yarcowie project.

Archer executive chairman Greg English said the results indicated the cobalt mineralisation extended over a “wide area” at the project where previous rock chip sampling returned cobalt grading between 0.36% and 0.94%.

Located in South Australia and only 20km east of Tesla’s Jamestown 100MW battery farm, Yarcowie has access to rail, power, gas and road.

Archer will integrate rock chip sampling and geophysical data to locate future exploration targets, which it plans to undertake in the coming months.

Ardea Resources (ASX: ARL)

Meanwhile, WA-focussed Ardea Resources is advancing a pre-feasibility study for the cobalt zone at its KNP project near Kalgoorlie.

The cobalt zone within KNP has a defined resource of 64.4 million tonnes grading 0.13% cobalt and 0.77% nickel.

As part of its pre-feasibility study, Ardea is looking at a 2 million tonne per annum operation which could produce up to 2,500tpa of cobalt-in-sulphate and 15,000tpa of nickel-in-sulphate.

KNP is also prospective for scandium, platinum, palladium, manganese, chromium and high purity alumina.

The company is investigating the potential of commercially extracting all the minerals and Ardea is funded through to the end of a definitive feasibility study at KNP.

Artemis Resources (ASX: ARV)

Perhaps better known for its Pilbara conglomerate gold assets Artemis Resources also wholly owns the Carlow Castle gold, copper and cobalt project in WA.

In April last year, the company revealed high grade cobalt intersections from exploration drilling at the project.

The program returned cobalt grading between 1.87% and 6.54%. Further drilling at Carlow during the year also offered up an 8m intersection with 0.34% cobalt, 9.9g/t gold and 2.85% copper.

Drilling at the project was ongoing with the company aiming to publish an updated JORC-compliant resource containing the cobalt credits by the end of last year.

Additionally, Artemis owns the Radio Hill processing plant and surrounding deposit, which is believed to contain cobalt as well as nickel and copper. A drilling program is underway at the deposit to test mineralisation at surface.

Auroch Minerals (ASX: AOU)

Auroch Minerals has three key projects in multiple regions prospective for cobalt, copper, zinc, and lithium.

The company is earning a 100% interest in the Tisova cobalt, copper and gold project in the Czech Republic. Auroch completed initial drilling at Tisova in late November and initial assays from grab sampling revealed cobalt grading up to 0.35%.

However, in its early January market announcement, Auroch chairman Glenn Whiddon said the assays were “disappointing” and not in line with the company’s expectations.

“While the results are not as hoped for, analysis of the drill core versus the previous grab samples suggest a different origin for the two sets of samples within the large Tisova deposit,” Mr Whiddon said.

“We believe this to be a logical explanation for the drilling results based upon the historical mining – dating back to 1600s,” he said.

He added the company believed the initial four drill holes had not hit the cobalt-rich portion of the orebody and the company will review its 3D model of sulphides and use geophysical methods in an attempt to identify further sulphide bodies.

According to Auroch, Tisova is in the heart of Europe’s industrial hub.

Auroch has until March 2018 to elect to proceed with the project acquisition.

Aus Tin Mining (ASX: ANW)

Aus Tin Mining is pursuing a cobalt zone at its 100%-owned Mt Cobalt project about 40km from Gympie in Queensland.

A 200m diamond drilling program was kicked-off in early December to test extensions to the historic cobalt and manganese mine where a 7m wide lode purportedly returned cobalt at an average 7.5% grade.

Nine reverse circulation holes were completed at the project in 2016 and produced a 7m interval grading 0.84% cobalt and another 7m interval grading 0.12% cobalt.

Aus Tin claims the its cobalt zone target is about 800m long and previously rock chip sampling at the project assayed up to 1.66% cobalt.

Australian Mines (ASX: AUZ)

One of the more popular stocks in various forums is Australian Mines, which just achieved 100% ownership of its flagship Sconi cobalt, nickel and scandium project in Queensland’s north.

About 250km from Townsville, Sconi has a resource of 89mt grading 0.11% cobalt and 0.80% nickel.

Trial mining was started at the end of September to produce 160kg of nickel sulphate, 20kg of cobalt and 5kg of scandium oxide.

Once produced, the minerals will be sent to potential off-take partners for assessment.

A bankable feasibility study is due for completion in April 2018.

According to the company, Sconi “is the most advanced project of its type in Australia” and has an estimated 20-year mine life.

Australian Mines secured a A$20 million placement in early November – giving the company enough cash to progress Sconi and its other cobalt, nickel, scandium project – Flemington in New South Wales. Flemington has an initial resource of 2.7 million tonnes grading 0.1% cobalt, 403 parts per million scandium. Australian Mines claims the Flemington maiden resource only encompasses about 1% of the identified prospective area.

Barra Resources (ASX: BAR)

Held under a 50:50 joint venture with Conico, Barra Resources is exploring the Mt Thirsty project which is an oxidised nickel laterite deposit with high cobalt values.

Situated in WA’s southern goldfields, Mt Thirsty has inferred and indicated resources of 31.9 million tonnes grading 0.13% cobalt, 0.55% nickel and 0.86% manganese.

According to Barra, the near surface Mt Thirsty deposit has the potential to emerge as one of the world’s top 10 cobalt suppliers.

The joint venture released a scoping study in October which revealed a 21-year mine life to produce up to 1,280tpa cobalt.

The study also estimated a A$212 million capital cost with a four-year pay back.

The project is close to rail, road, power, water and port infrastructure.

Berkut Minerals (ASX: BMT)

Focussed on exploring for cobalt in Scandinavia, Perth-based Berkut Minerals owns 100% of the Skuterud project in Norway which encompasses 1,250 hectares within 100km of Oslo’s port. The region also hosts one of the world’s most well-known historic mines Skutterudite which was operated throughout 18th and 19th Centuries.

As well as Skuterud, Berkut has more than 300 hectares of granted licences in Sweden’s Gladhammer and Tunaberg regions where cobalt was mined between 15th and 19th Centuries.

Berkut said it has selected Europe as the region to undertake cobalt exploration, due to the area’s high electric vehicle uptake.

The company claims it has potential nearby end-users in the region’s four operational lithium-ion battery factories, with five more in the pipeline.

By late November, Berkut had almost completed its maiden seven-hole diamond drill program at Skuterud and several assay results were released in early January.

Better intercepts included 2m grading 0.12% cobalt and 0.11% copper and 1m grading 0.16% cobalt and 0.11% copper.

The company said every hole intersected cobalt, with numerous intervals terminating in mineralisation. Berkut plans to continue exploring at Skuterud and its other cobalt prospects during 2018.

Blackstone Minerals (ASX: BSX)

Blackstone Minerals is exploring for cobalt and gold at its recently acquired Little Gem project in Canada’s British Columbia region.

The company entered a binding agreement to purchase the project in late July and has since acquired more ground near the project in early November – increasing its strike target from 12km to more than 48km.

Including the November ground acquisition, Little Gem totals 335 square kilometres and rock chip samples have uncovered 6.2% cobalt and 46g/t gold.

The company also reported cobalt grades of 5.7% and 4.4% from sampling carried out as part of its due diligence to acquire Little Gem.

Blackstone completed a A$5 million share placement in mid-December to fund advancing Little Gem.

In early January, the company’s first drill hole returned a 4.3m intersection with 1% cobalt and 15g/t gold, including a 1.1m interval grading 3% cobalt and 4.4g/t gold.

Once the winter weather has eased, Blackstone plans to resume its maiden drilling program in the June quarter to investigate the mineralisation further and test potential extensions.

Blina Minerals (ASX: BDI)

Another newcomer to the cobalt space is Blina Minerals which has agreed to acquire a 100% interest in the 29sq km La Cobaltera project in Chile.

The project lies within a historic cobalt producing region and includes a processing plant and tailings dumps.

Blina immediately started preliminary exploration across the project including mapping for targets and rock chip sampling.

The company’s priority was to generate targets for its maiden drilling program which it plans to undertake once it has completed its four months due diligence period which is up at the end of February.

Cape Lambert Resources (ASX: CFE)

Cape Lambert Resources has a 70% interest in the Kipushi cobalt tailings project in the DRC and plans to increase the interest to 80%.

To process the ore, Cape Lambert owns 100% of the Kipushi plant, which requires refurbishment for optimal copper and cobalt processing.

Cape Lambert is currently in discussions regarding funding the refurbishment and potential offtake agreements for its copper and cobalt ore. The company appointed adviser Metals Risk Management to assist with finalising these negotiations.

The company also has an agreement in place to acquire 70% of Australian Mining Company Zambia which owns the Kitwe cobalt copper tailings project in Zambia.

In mid-2017, Cape Lambert agreed to sell 100% of its rights in the Kasombo copper cobalt project in DRC to ASX-listed Fe Limited. Despite the sale, Cape Lambert retains an interest in the project via its 58% interest in FE.

Castillo Copper (ASX: CCZ)

Base metals explorer Castillo Copper is investigating cobalt potential at several projects including Broken Hill, Mt Oxide, and Marlborough.

Broken Hill is about 20km from its namesake town in NSW and the company has identified four cobalt zones.

In November, Castillo announced it was ramping up cobalt exploration to take advantage of the burgeoning electric vehicle and sustainable energy markets.

A legacy desktop review revealed four target areas, with readings inside and just outside of the tenements returning between 0.20% and 0.70% cobalt.

Over at Marlborough in Queensland, historic government data identified cobalt grading about 0.06% in the region.

Another desk top review, this time at Mt Oxide, returned up to 0.09% cobalt in the area. The company hopes to announce a maiden resource by mid-2018.

Celsius Resources (ASX: CLA)

Celsius Resources finished its 14,000m resource drilling campaign in mid-December for its Opuwo project in Namibia.

The latest assay batch which was announced in late December revealed the known mineralisation at Opuwo had been extended at depth.

A down dip extension of 4m grading 0.13% cobalt and 0.40% copper was identified – similar to previously reported near-surface results.

Opuwo covers about 1,470sq km in Namibia’s north west. The project is approximately 30km from the Opuwo town which provides multiple services including sealed roads, accommodation, fuel, supplies, airport and hospital.

Additionally, the country’s main power station is close to Opuwo, with a 66kV transmission line running across the project’s eastern boundary.

A resource is scheduled for release in February, with Celsius’ managing director Brendan Borg claiming the project would be “rapidly” advanced in 2018.

Clean TeQ (ASX: CLQ)

Clean TeQ has its wholly-owned Sunrise nickel, cobalt and scandium project in NSW.

The company claims Sunrise, formerly known as Syerston, is one of the world’s highest grade and biggest nickel and cobalt deposits outside of the Africa.

A definitive feasibility study on the project is underway and due for completion by the end of March. The study is investigating the viability of using Clean TeQ’s proprietary processing technology to concentrate the ore for the rapidly growing lithium-ion battery market.

In anticipation of the study’s results the company has been planning for the construction phase including purchasing an expandable 300-person accommodation facility. The company aims to begin project construction mid-year.

The project has existing ore reserves of 96 million tonnes grading 0.65% nickel and 0.10% which could support a 39-year operation.

Cobalt Blue Holdings (ASX: COB)

NSW-focused Cobalt Blue is carrying out a resource upgrade drilling program at the 63sq km Thackaringa cobalt project, about 20km from Broken Hill and in proximity to necessary infrastructure.

Better results announced in December from the program included 72m grading 0.11% cobalt, 10.1% sulphur and 9.8% iron; 41m grading 0.10% cobalt, 10.4% sulphur and 10% iron; and 25m grading 0.12% cobalt, 9.5% sulphur and 10.6% iron.

A resource upgrade scheduled for release by April 2018.

In addition to drilling, Cobalt Blue is carrying out a pre-feasibility study, which is investigating producing a battery-ready cobalt product using calcine and leach processing. To-date, the company has been “delighted” with its testwork results.

Cobalt Blue anticipates the feasibility study will be delivered by mid-2018, with a bankable feasibility study and project approvals planned for mid-2019, followed by a decision to mine and acquiring requisite development finance.

Broken Hill Prospecting owns the tenements which Cobalt Blue is farming in to acquire the full 100%.

Collerina Cobalt (ASX: CLL)

A pre-feasibility study is underway at Collerina Cobalt’s namesake wholly-owned Collerina project in NSW.

Drilling at the 224sq km Collerina project has uncovered high grade cobalt zones with better intercepts returning 4m at 0.70% cobalt and 2m at 1.02% cobalt.

The project’s primary deposit Homeville hosts several types of mineralisation and Collerina has just begun a metallurgical program to produce 99.99% high purity alumina, as well as cobalt, nickel and manganese from the ore.

The testwork data will be incorporated into the pre-feasibility study which is due for completion by the end of June 2018.

Homeville has a current JORC-compliant resource of 16.3mt grading 0.93% nickel, 0.05% cobalt, 19% iron and 3.1% aluminium.

Conico (ASX: CNJ)

Conico owns 50% in the Mt Thirsty cobalt project in WA, with Barra Resources holding the other 50%.

Mt Thirsty is Conico’s flagship and sole project, which it is developing in conjunction with Barra.

For further information on Mt Thirsty, refer to Barra above.

Corazon Mining (ASX: CZN)

Corazon Mining is exploring for cobalt in Australia at its Mount Gilmore project in NSW.

According to the company, its Cobalt Ridge prospect is one of Australia’s highest-grade cobalt deposits.

In early December, Corazon reported assays from four drill holes at Cobalt Ridge had returned up to 1.37% cobalt.

The company said the drilling campaign had identified multiple cobalt, copper and gold mineralised trends.

Additionally, conventional flotation testwork on ore from Cobalt Ridge managed to recover 93.6% cobalt and 98.4% copper, which are amenable to simple procession options.

Future exploration will test Cobalt Ridge mineralisation to the south and east.

Cougar Metals (ASX: CGM)

Multi-metals explorer Cougar Metals owns the cobalt and nickel rights to the Pyke Hill project in Leonora in Western Australia.

Pyke Hill has a 2008 resource estimate of 14.7mt at 0.9% nickel and 0.06% cobalt and is about 40km from Glencore’s Murrin Murrin nickel operations.

Previous exploration has closed the resource off in all directions. As a result, the company believes further drilling won’t make a substantial difference to the resource figure.

No recent exploration has been undertaken at Pyke Hill and Cougar is seeking to sell the project or set up a joint venture arrangement with third parties.

At this stage, Cougar is focussed on advancing its Toamasina graphite project in Madagascar.

European Cobalt (ASX: EUC)

Another stock popular with the investors is European Cobalt, which is focussed on its 100%-owned Dobsina project in central Slovakia. Dobsina hosts multiple historical mines across the Zemberg vein systems that produced an average cobalt grade of 4% between 1780 and the 19th Century.

Since acquiring the project in late April 2017, European Cobalt has been actively exploring and reported multiple high-grade, cobalt, nickel and copper discoveries at targets including waste dumps within the project.

At the end of October, a road cutting from Dobsina returned cobalt grading up to 7.3%. In late December, the company reported initial assays from four diamond drill holes at the project, including a 1m intersection grading 0.23% cobalt and 0.36% nickel. The intersection comprised a 0.6m interval with 0.31% cobalt and 0.16% nickel.

In the first six months of 2018, the company plans to carry out surface drilling at its Joremeny targets while completing underground refurbishment of the historical Joremeny adit.

Further field reconnaissance, geotechnical assessments and metallurgical testwork will also be undertaken.

The project is also near to power, water and rail.

FE Limited (ASX: FEL)

Multi-commodity explorer Fe entered the cobalt space in mid-2017 when it agreed to acquire 100% of Cape Lambert’s rights to Kasombo copper and cobalt project in the DRC.

Encompassing 600 hectares, Kasombo includes two granted mining licences and the company completed preliminary drilling in early January.

Two reverse circulation holes were drilled at the Kasombo 5 prospect which is believed more prospective for copper. Four RC holes were completed at the Kasombo 7 prospect which is anticipated to be higher in cobalt mineralisation.

mPrevious sampling at the project returned cobalt grading up to 6.99%.

Assays from the drilling are currently pending.

First Cobalt (ASX: FCC)

Canada-focussed First Cobalt has given itself the title of the “largest cobalt exploration in the world”.

Debuting on the ASX on the 29 November 2017, First Cobalt has been an unstoppable force, completing two company acquisitions (CobalTech and Cobalt One) in early December, followed by another property acquisition and a A$30 million placement. And that was just December. The new year heralded another landholding acquisition, with three of the claims near to the company’s existing projects, in Ontario’s northern Cobalt Camp region.

First Cobalt is the largest landholder in Canada’s Cobalt Camp, controlling more than 10,000 hectares of tenure, which includes 50 historic mining operations and North America’s only permitted cobalt refinery to produce battery materials.

Commenting on the company’s recent activities, First Cobalt chief executive officer and president Trent Mell said First Cobalt was now the “largest cobalt exploration company in the world”.

He added First Cobalt now controlled almost half of “the most prospective cobalt district outside of the Democratic Republic of Congo”.

Golden Deeps (ASX: GED)

Golden Deeps emerged from a trading halt in early December last year to report it had entered a binding agreement to acquire 100% of two cobalt projects in Ontario, Canada.

The projects Professor and Waldman are both in the southern section of Ontario’s Cobalt Mining Camp region and host historic mines.

Between 1910 and 1930, 2,066 pounds of cobalt was produced from Waldman. While carrying out due diligence at Waldman, Golden Deeps identified the decline into the mine remained open and could potentially be refurbished.

The company also claims the infrastructure around the mine remains in a good condition.

As part of the acquisition, Golden Deeps is carrying out technical and legal due diligence at both projects.

Once electing to complete the acquisition, Golden Deeps plans to conduct geophysical exploration as well as compiling historical data, surface sampling and trenching.

The company was planning to begin its fieldwork early this year, with the first drilling program to finish during the June to August summer months.

GME Resources (ASX: GME)

Also exploring near Murrin Murrin is GME Resources, which is advancing its wholly-owned NiWest nickel and cobalt project in WA.

The nickel and cobalt mineralisation is shallow, and the company has calculated a measured, indicated and inferred JORC-compliant resource for the project of 81mt grading 1.03% nickel and 0.06% cobalt equating to about 830,000t of nickel and 52,000t of cobalt.

During the second half of 2017, GME was focussed on its metallurgical testwork to produce high purity nickel and cobalt for the battery sector.

Further testing is underway to develop an optimised cobalt recovery flowsheet to produce cobalt products for various end-users.

Hammer Metals (ASX: HMX)

Hammer Metals owns 100% of the Millennium copper and cobalt project near Cloncurry in Queensland, where TSXV-listed Global Energy Metals Corporation is performing a staged earn-in after executing an agreement in late September last year.

Under the agreement between Global Energy Metals Corporation and Hammer, Global Energy Metals Corporation has a three-year option to earn up to 75% in Millennium by spending A$2.7 million on exploration including a A$250,000 cash payment.

The project’s namesake deposit has a maiden inferred resource of 3.07mt grading 0.14% cobalt, 0.35% copper and 0.12g/t gold.

During its 2016 reverse circulation drilling program, Hammer reported intercepts of 19m grading 0.38% cobalt, 1.27% copper, 0.70g/t gold, and 33m grading 0.16% cobalt, 0.66% copper and 0.34g/t gold.

Global Energy Metals Corporation began its phase one work program at Millennium to boost the resource and test extensions to mineralisation.

The company will also drill out cobalt targets to the project’s north as well as further scoping studies.

Havilah Resources (ASX: HAV)

Multi-commodity explorer Havilah Resources is advancing its Mutooroo copper-cobalt project about 60km west of Broken Hill in South Australia.

According to Havilah, Mutooroo comprises South Australia’s only JORC-compliant cobalt resource which includes 17,540t of contained cobalt.

To gain maximum value from its cobalt credits, Havilah is investigating the option of developing a 500,000tpa roaster and sulphuric acid plant to recover the cobalt along with copper and gold.

Initial mine planning comprises a seven-year operation with 500,000tpa throughput. However, there is potential to increase production by deepening the open pit or extend mining along strike.

Jervois Mining (ASX: JRV)

Jervois Mining plans to fast-track its 100%-owned flagship Young cobalt and nickel project (Nico Young) in NSW.

After a review of historical data, the company published a JORC-compliant resource upgrade in late November 2017 which revealed 167.8mt grading 0.59% nickel and 0.06% cobalt, and includes 33.4mt grading 0.66% nickel and 0.12% cobalt.

Located in an established mining and farming region, Nico Young comprises two exploration licences close to the town of Young which has a population of 7,000.

Due to its proximity to the town, Nico Young has access to gas, rail and major roads. Jervois has started early environmental activities and landholder negotiations.

The company has also begun studying heap leach processing of Nico Young ore to create battery-grade concentrator for manufacturers. According to Jervois, heap leach processing has lower capital and operational costs than high pressure acid leach processing.

Longford Resources (ASX: LFR)

Longford Resources executed an agreement with American Manganese in early November to secure an initial 60% interest in the Hazelton cobalt, copper and gold project in Canada’s British Columbia.

Hazelton covers 10sq km hosts three historic mines including Victoria which averaged 2.8% cobalt and 123.4g/t gold. Other mines were Rocher Deboule which yielded grades of 5.9% copper and 2.9g/t gold, and the Highland Boy mine where ore grades were about 7% copper and 1.8g/t gold.

There has been little exploration at the project since the mines last operated in 1952.

Due diligence was completed in late December with Longford electing to proceed with the acquisition.

Hazelton builds on Longford’s existing cobalt portfolio which includes Colson and Goodsprings – both in the US.

Assays from sampling historic underground workings at Colson returned 2.5m grading 5.33% copper, 0.59% cobalt and 2.24g/t gold while ore grading up to 29% cobalt was previously shipped from the Columbia mine within Goodsprings.

Metalicity (ASX: MCT)

Focussed on advancing its Admiral Bay zinc project in WA’s Kimberley, Metalicity also owns the Kyarra cobalt project – also in WA.

During the September quarter last year, Metalicity completed its first drilling program comprising 1,800m. Assays revealed cobalt was intersected in every hole returning up to 0.014%.

At the time of writing, Metalicity was working with CSA Global to plan the next exploration stage at Kyarra.

Meteoric Resources (ASX: MEI)

Canada-focussed Meteoric Resources has been carrying out initial sampling at its Mulligan project in Ontario, which is about 50km north of the Cobalt Mining Camp region where cobalt product had an average 10% grade.

Assays on 13 December 2017 returned up to 9.71% cobalt from rock chip samples.

The Ontario Department of Mines and Conwest Exploration previously identified cobalt grading 12.6% and 19%, respectively, as well as nickel and gold mineralisation.

In late November, Meteoric announced its plan to raise A$4.34 million to fund its 2018 exploration activities at Mulligan and its two other Canadian projects Iron Mask and Midrim.

The other two projects are also polymetallic and prospective for nickel, copper, platinum group metals, cobalt, silver and gold.

According to Meteoric, Mulligan’s geological setting and mineralisation is similar to the Cobalt Mining Camp polymetallic mineralisation, which is Canada’s most prospective known cobalt province producing more than 40 million pounds of the metal and 450 million ounces of silver.

Marquee Resources (ASX: MQR)

Cobalt newbie, Marquee Resources has secured an agreement in early December last year to acquire three exploration projects in Canada: Werner Lake, Werner Lake East/West and Skeleton Lake.

Werner Lake is located in Ontario – a known region for cobalt prospectivity. The project has an indicated mineral resource of 79,400 tonnes grading 0.43% cobalt, with the mineralisation remaining open in all directions. Previous mining at the project pulled out about 143,386 pounds of cobalt at an average grades of 2.2%.

Under the agreement with various venders, Marquee can gain up to a 70% stake in Werner Lake by achieving several milestones, and a 100% stake in both Werner Lake East/West and Skeleton projects.

Werner Lake East/West comprises about 18.4sq km of prospective cobalt territory and Skeleton encompasses 14.08sq km and is 55km north of the town Cobalt in Ontario.

At the time of writing, Marquee Resources was undertaking its 60 days due diligence prior to committing to the purchases.

MetalsTech (ASX: MTC)

Although primarily a lithium play MetalsTech collared a 100% interest in the Bay Lake cobalt project in Canada in April last year.

Comprising 3,200 hectares, the project is 10km from Ontario’s Cobalt town.

Early sampling at the project returned 1.17% cobalt and 7.7 grams per tonne silver from a surface dump pile at the Van Chester prospect.

MetalsTech’s wholly-owned subsidiary iCobalt executed an agreement to purchase the Rusty Lake cobalt, silver mine in Ontario in late November.

The project includes the historic Rusty Lake mine and encompasses 816 hectares and 52 mining claims.

Recent surface sampling at Rusty Lake yielded up to 11.85% cobalt, with multiple other samples grading above 5%.

In late December, MetalsTech reported iCobalt would purchase Bay Lake and seek admission to the ASX.

The iCobalt spinout is due to complete by the end of March and iCobalt will advance exploration at Bay Lake and Rusty Lake once due diligence has been finalised and the company has exercised its purchase option.

MetalsTech plans to retain a 33% stake in the entity.

Northern Cobalt (ASX: N27)

Northern Cobalt is rapidly advancing its Wollogorang project in the Northern Territory.

Northern Cobalt has reported multiple high-grade cobalt assays from its almost 150-hole drilling campaign at the project.

Assays returned in early December 2017 included a 1m interval grading 2.33% cobalt, 0.45% copper and 1.01% nickel.

To-date, 70 RC and 10 diamond core holes have been drilled at the Stanton deposit to upgrade the current JORC-compliant inferred mineral resource of 500,000 tonnes of 0.17% cobalt, 0.09% nickel and 0.11% copper. Further assays are due in batches through to February 2018.

In late December, Northern Cobalt obtained an airborne magnetic survey covering Stanton and surrounding prospects and encompassing 90sq km of ground.

Analysis of the survey data has revealed several magnetic anomalies with similar characteristics to Stanton.

An updated inferred resource is scheduled for release by the end of March 2018, with a further resource upgrade to indicated status due by the end of June, once the company has access to the metallurgical results.

According to the Northern Cobalt, the cobalt mineralisation identified so far at Wollogorang is predominantly cobalt sulphide and non-refractory – meaning it won’t require roasting leading to lower capital and operating expenditure.

Located in the Northern Territory’s north east, Wollogorang is situated between two potential ports, which are accessible by sealed road.

Nzuri Copper (ASX: NZC)

Nzuri Copper is exploring for copper and cobalt along Africa’s copper belt in the DRC. A recently completed feasibility study into the company’s flagship Kalongwe copper and cobalt project has estimated up to 1,507tpa of cobalt and 19,360t of copper production over a seven-year, open pit operation.

Kalongwe has reserves of 6.98 million tonnes grading 3.03% copper and 0.36% copper, with the cobalt amenable to simple leach processing. The project’s near-surface resources amount to 42,700t of contained cobalt and 302,000t of copper.

Nzuri owns 85% of the project which is fully permitted with a 12-month timeline to production after receiving final funding and board approvals.

Additionally, the company has identified opportunities to enhance the project’s economics and mine life via staged expansion including the addition of leaching solutions for cobalt ore which will initially be stockpiled.

Nzuri also is acquiring a 98% stake in the Fold and Thrust Belt Joint Venture project which comprises 334sq km of copper and cobalt prospective landholding where the company is actively exploring.

In early January, China-based Huayou Cobalt completed its A$10 million investment in Nzuri – boosting its interest in the company to almost 15%.

Pioneer Resources (ASX: PIO)

Pioneer Resources is exploring for cobalt and nickel at its 100% owned Gold Ridge project only 35km from Kalgoorlie in WA.

The project comprises 29sq km and includes the Blair Nickel mine which was closed in 2008 after producing 1.26mt of nickel.

During 2017, Pioneer reviewed the project for cobalt content and identified multiple shallow targets for drilling.

Historical exploration identified cobalt intersections across the project area including 14m grading 0.211% cobalt, 9m grading 0.373% cobalt and 30m grading 0.147% cobalt.

At the end of November 2017, Pioneer Resources kicked-off a 30 RC hole drilling campaign, with assays from the campaign due by late January.

Samples will also be tested for alternative metallurgical processing methods to extract the both nickel and cobalt.

Platina Resources (ASX: PGM)

Platina Resources’ flagship Owendale in central NSW is one of the world’s largest and highest-grade scandium projects, which has multiple mineral credits including cobalt, platinum and nickel.

In September 2017, Platina published a maiden reserve for Owendale including 17.6mt grading 310ppm scandium, 0.12% cobalt, 0.30g/t platinum and 0.23% nickel. The project’s total measured, indicated and inferred resource sits at 33.7mt grading 395ppm scandium, 0.06% cobalt, 0.28g/t platinum and 0.11% nickel.

Situated only 7km from Clean Teq’s Sunrise cobalt and scandium project and in proximity to rail and electricity, the Owendale resource is shallow and continuous. A pre-feasibility study was completed in mid-2017, revealing a possible 44-year mine life with an initial A$94 million capital cost and annual revenue of A$58 million.

A definitive feasibility study is underway and due for completion in the latter half of 2018.

Riedel Resources (ASX: RIE)

European energy metal focussed Riedel Resources is exploring the Carmenes cobalt and copper project in Spain’s north.

The company completed its project due diligence in early November after executing a staged earn-in agreement to eventually acquire up to 100% of the approximately 40 sq km project in July last year.

Carmenes contains a number of high grade historical mines where mining produced 38,000t of concentrate containing cobalt concentrate grades up to 14% cobalt and copper concentrate grades up to 33% copper.

According to Riedel, 95% of the project area has not been tested with modern exploration, presenting a significant opportunity for the company.

Since completing due diligence, Riedel has been fast-tracking exploration at the project by conducting radiometric surveys, magnetics, IP surveys and rock chip sampling in mid-December.

At the time of writing, assays were pending from the encouraging rock chip sampling program.

Red Mountain Mining (ASX: RMX)

Focussed on its Mokabe-Kasiri cobalt and copper project in the Democratic Republic of Congo, Red Mountain Mining has just completed its 2017 exploration program.

About 70km north of one of the world’s largest copper-cobalt mines Tenke Fungurume, the Mokabe project encompasses 130sq km and includes 17 artisanal licences.

The exploration program involved collecting 657 soil and rock chip samples were sent off for analysis.

Cobalt drilling results were pending at the time of writing from a rotary air blast drilling program totalling 50 holes.

However, earlier grab samples returned up to 2.9% cobalt.

Mokabe-Kasiri has access to road, power and water.

St George Mining (ASX: SGQ)

After exploring for nickel and copper, St George Mining reported the presence of cobalt at its Mt Alexander project in WA.

Assays from a recent drilling program at the project’s Stricklands deposit revealed a 17.45m intersection at 3.01% nickel, 1.31% copper and a 0.13% cobalt. The intersection included a 5.3m interval with 0.21% cobalt.

Previous exploration at the project identified cobalt at other sites which returned 0.20% cobalt and 0.16% cobalt.

In early January, St George published drill results from its Cathedrals prospect which revealed a 3.28m intersection grading 5.77% nickel, 2.43% copper, 0.18% cobalt and 5.05g/t platinum group elements. The intersection included a 1.9m high grade interval with 7.42% nickel, 3.45% copper, 0.23% cobalt and 5.61g/t platinum group elements.

Further drilling during early 2018 will test the extent of the Stricklands mineralisation and other targets at Mt Alexander.

Mt Alexander includes four granted exploration licences, with the recent Strickland and Cathedrals Belt discoveries on the exploration licence held under a joint venture with Western Areas (ASX: WSA), where St George owns 75% and Western Areas retains a 25% non-contributing interest.

The project has access to nearby processing plants as well as existing infrastructure.

Trek Metals (ASX: TKM)

Another new entrant into the cobalt space, Trek Metals gained seven lithium and cobalt exploration applications, known as the Arunta lithium-cobalt project, through its takeover of Elm Resources in mid-November. The licences encompass 5,274sq km and are about 200km north of Alice Springs.

Additionally, a major unsealed road connects the project area to the Stuart Highway.

Historical rock chip samples across the tenements in the Northern Territory returned up to 0.12% cobalt and 0.15% lithium.

Field work was undertaken along with ongoing historical data compilation. Once the tenements have been granted, initial ground exploration work is planned for 2018.

Victory Mines (ASX: VIC)

In mid-November Victory Mines emerged from a trading halt with news it had executed an agreement to acquire four projects prospective for cobalt across NSW and WA.

As part of its due diligence process for acquiring the NSW projects, Victory engaged a geology team to undertake a review of the projects and compare them to Platina, Australian Mines and Clean TeQ’s nearby tenements.

The geology team informed Victory there was a “strong indication” mineralisation was present at the NSW Husky and Malamute projects.

The two WA projects Peperill Hill and Galah Well are in areas known for cobalt prospectivity, with historic exploration returning 0.24% cobalt at Galah Well and 0.73% cobalt at Peperill Hill.

All projects are in proximity to power, roads and a local labour pool.

Winmar Resources (ASX: WFE)

In early December, Winmar Resources edged into the cobalt space after executing an agreement to hooking three bocks with mining claims across 2,240 of cobalt prospective land in Ontario, Canada.

According to Winmar, Ontario’s Gowganda mining district is one of the most cobalt and silver prospective regions outside of the DRC.

The claims are close to high-grade silver and cobalt deposits that had been historically mined for their silver contact between 1910 and 1989.

By the end of 1969, an estimated 60.2 million ounces of silver and 1.3 million pounds of cobalt had been extracted from the area.

Reviews of historic grab samples from the Boom Lake block returned cobalt grading up to 0.9%

As part of the acquisition, Winmar had until 22 December to complete due diligence and a 12-month option period to purchase the United Reef and Calcite Lake blocks.

What other minerals stand to benefit?

In addition to cobalt and lithium, nickel and graphite are critical commodities for most lithium-ion battery formulas.

More detailed information on the rapidly expanding lithium-ion battery industry, other associated minerals, and their market fundamentals can be found here.

SEE ALSO:

– Gold stocks on the ASX

– Silver stocks on the ASX

– Lithium stocks on the ASX

– Graphite stocks on the ASX

**– Zinc stocks on the ASX

– Nickel stocks on the ASX

– Rare earth stocks on the ASX

****– Vanadium stocks on the ASX

– Uranium stocks on the ASX

– Mineral sands stocks on the ASX

– High Purity Alumina stocks on the ASX

– Tin stocks on the ASX

– Tungsten stocks on the ASX

– Hydrogen stocks on the ASX

– Oil and gas stocks on the ASX

**– Cannabis stocks on the ASX

Get the wire before the market opens.

The ASX small-cap stories that matter, filed before 9am AEST. Curated by the Small Caps desk.