The new age energy storage bandwagon has quite possibly hit the buffers, courtesy of a legislative amendment in the polymetallic-rich Democratic Republic of Congo (DRC).

The DRC’s parliament voted to repeal cornerstone mining law imposed in 2002 giving resource companies a secure operational space guaranteeing tax-free operations for at least 10 years.

The slew of law amendments announced by the DRC on 27 January includes a tax hike from 2% to 3.5% on all mining, the removal or previously-expected tax amnesties and the introduction of a so-called “super profits tax” of 50% if commodity prices rise by 25% over-and-above what was estimated in resource feasibility studies.

Given the sharp increase in cobalt, lithium, copper and gold prices since 2016, the law changes effectively open-up existing mining companies based in the DRC to a significantly higher tax burden and sudden intangible uncertainty within billion-dollar projects currently in mid-construction.

It is feared the law changes will push some projects outside of economic viability and throws doubt on how profitable large miners such a Glencore, BHP and Ivanhoe can be in the DRC.

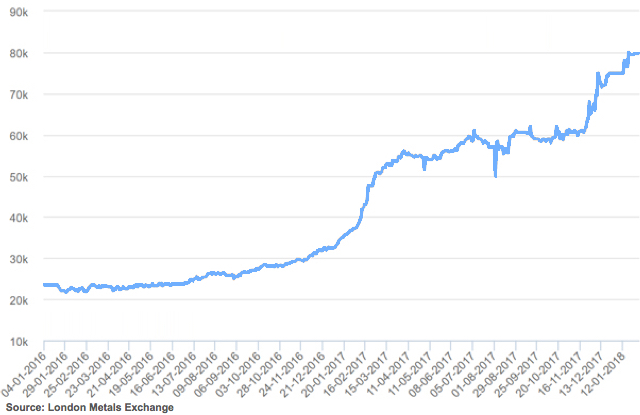

Cobalt prices have blitzed all analyst estimates, growing from around $20,000 per tonne in January 2016 to around $80,000 today – making the DRC’s law changes uniquely influential and hard-hitting for global commodity markets.

The new legislation directly impacts large miners first and foremost given their comparatively larger mining volumes and operating profit margins; with energy shares reeling since the legislative announcement.

DRC market impact

The largest foreign miner in the DRC, Glencore (LSE: GLEN) has seen its shares drop 8.2%, Ivanhoe Mines (TSX: IVN), the largest copper producer in the DRC and currently developing what analysts have dubbed “the most important copper deposit in human history” has fallen 25%. Randgold Resources (LSE: RRS), operator of the $2.5 billion Kibali gold mine, is currently down 3%.

However, not all DRC-based resource companies had a bad field day last week.

Micro-capped Red Mountain Mining (ASX: RMX), currently progressing its Mokabe-Kasiri cobalt and copper project in the DRC, managed to close the week 9% higher with other smaller explorers managing to dodge much of the fear-based selling on global markets in late Friday trade.

Having listed on the ASX last year, Northern Cobalt (ASX: N27) is already expediting its development by fast-tracking resource drilling at its cobalt project in the Northern Territories of Australia, close to where Rio Tinto was targeting copper in the mid-1990s.

Northern Cobalt recently announced results from an extensive drilling program and hopes to fill any supply gaps that the DRC may be on its way to creating.

Other ASX-listed companies could potentially benefit from the unrest in the DRC.

It is hoped that junior explorers may be able to strafe the brunt of the effects of the tax-law changes currently weighing on larger miners such as Glencore and Ivanhoe, given their smaller size and smaller operational budgets.

Regardless, the future of mining in DRC has been steeped in further uncertainty for everyone, and yet, the DRC has access to more battery metals than any other country in the world.

The cobalt problem in the Congo

By a country mile, the majority of the world’s cobalt is sourced from the DRC. According to the US Geological Survey, the DRC contributed 66,000 tonnes to global cobalt supplies in 2016, around half of the world’s total production of around 123,000 tonnes.

About $10 billion worth of cobalt is exported from the DRC each year and if mining conditions were favourable, this export amount could potentially rise by several multiples given how well-endowed with metals the DRC is, and how quickly metals prices are rising on the back of consumer demand.

The DRC is a key global player in the lithium-ion battery production cycle by virtue of its natural resource endowment, but its tax-law changes, human rights abuses and poor mining law standards are making it more difficult for foreign miners to commit to long-term projects that reap the highest volumes of high-grade metals.

Why cobalt, why lithium, and why now?

Lithium-ion batteries have taken the world by storm in the modern-day world of electric vehicles and efficient energy-storage.

A battery-supported shift in how energy is sourced and consumed is gradually making its way onto world markets as Tesla’s record sales of electric vehicles are proving – with cobalt and lithium being the two key components.

The fly in the soup is the DRC with its questionable internal politics, mining law and human rights abuses that have raised the attention of large manufacturers such as Apple and Panasonic to publicly denounce the DRC, as a non-viable source for the raw materials in their products.

The sharp increases in cobalt and lithium demand in recent years have put pressure on production supply routes and brought to the surface an unsightly problem bellowing in the underbelly of African resource exploration – an unstable political climate with debilitating effects of civil war, poor living conditions and archaic mining standards.

The BBC has termed DRC’s domestic troubles as “Africa’s world war” that has claimed over 5 million lives as a direct result of fighting or because of disease and malnutrition, and says “these effects were fuelled by the DRC’s mineral wealth”.

Almost overnight, lithium and cobalt have become a conflict metals courtesy of the DRC with PR-conscious juggernaut cobalt/lithium consumers such as Tesla, Panasonic and Apple publicly refusing to be associated with DRC’s cobalt laden-mines.

Grass roots support for lithium-ion energy storage

If consumers clamouring for battery-powered devices wasn’t enough of a demand-side factor, there is also the public sector – the switch to cleaner and more efficient electric vehicles slowly but surely becoming legislative.

European countries are sequentially waking up to the benefits of electric cars and mandating electric vehicles directly into law with the Netherlands leading the charge.

Dutch legislators have mandated all new cars to be electric by 2025, France is sequentially phasing out petrol-powered cars and Germany is also considering similar legislation aimed at making EV’s more widely adopted.

China is also on track to be producing more electric than petrol cars each year by 2023.

It would seem the commercial world of industry and consumption is ready to ride off into the digital wonderland fuelled by cobalt-infused lithium batteries, but the DRC has the ignition key and it’s treating the whole scenario as a profit-bearing taxi journey.

Alternative cobalt sources on the horizon

As Small Caps reported last month, the DRC’s imposed tax changes are likely to induce hastier resource exploration in other areas around the world by resource companies that may have previously considered the DRC as a viable mining location.

The enactment of DRC’s tax laws was quite possibly the formalisation of what many analysts were expecting for several months – especially when the DRC has a capital-intensive national election to proceed with in December.

Given the DRC’s previous political record, sceptics are claiming the DRC’s treasury-chest-boosting mining tax is a sneaky move by the incumbent government to maintain its power-grip within the country.

The political musical chairs in the DRC will come to an end eventually, but the uncertainty surrounding the DRC’s polymetallic supply capability will likely not.

This could pose a problem for lithium-ion battery adoption globally but the opportunity is also clear: high-grade cobalt supplies in other locations with more politically-friendly mining conditions have been given a huge boost, and a huge emulation target to boot.