- 01Oil spike, Hormuz risk, repricing.

- 02Mid East conflict disrupts energy flows.

- 03ASX200: risk and inflation shift pricing.

- 04BWP, DRR, BSL, BGA, MPL near breakout.

If there is one moment this year to pay close attention to markets, it is now.

Oil has surged past US$120 per barrel in recent weeks before pulling back. Global supply routes are under strain. Central banks are being forced into difficult decisions. And equity markets, including Australia, are starting to reflect a very different set of assumptions about growth, inflation and risk.

In this note, we walk through what is really driving markets today, how the energy shock is feeding into inflation and policy, and what it means for the outlook of the ASX 200.

Most importantly, we highlight five high-quality ASX-listed companies that, in our view, are currently undervalued and approaching a potential technical breakout.

In an environment where broad exposure is no longer enough, identifying the right opportunities matters more than ever.

The global economy in early May 2026 is navigating a phase that is both historically rare and structurally consequential. What stands out is not simply the scale of disruption, but the way multiple shocks are unfolding simultaneously across geopolitics, energy systems and financial markets.

These forces are not isolated. They are reinforcing one another, creating a feedback loop that is redefining how risk is priced, how capital is allocated and how policymakers respond.

At the centre of this shift sits the escalation of hostilities in the Middle East, specifically the conflict involving the United States, Israel and Iran that began on February 28, 2026.

The strategic importance of the Strait of Hormuz has long been recognised, but what was once a theoretical vulnerability has now become a tangible constraint on global energy flows. With roughly 20% to 35% of the world’s seaborne oil and liquefied natural gas moving through this corridor, any disruption carries immediate and far-reaching consequences.

What we are witnessing is not a conventional supply shock. It is a structural interruption of the world’s most critical energy artery, combined with a breakdown in assumptions that have underpinned globalisation for decades.

The result is a broad repricing of financial risk that extends well beyond energy markets. Equity valuations, bond yields, currencies and corporate investment decisions are all being recalibrated against a more uncertain baseline.

Energy Markets Under Strain

As of May 4, 2026, energy markets remain volatile, even after a modest pullback from recent highs.

Brent crude, which reached US$126 per barrel in late April, is now trading around US$107.74. West Texas Intermediate sits near US$101.

While this easing offers some relief, we would caution against interpreting it as a sign of stability. The recent decline is largely a response to policy signalling rather than a shift in underlying fundamentals.

The United States has pledged to escort neutral vessels through the Strait of Hormuz, which has temporarily improved sentiment. However, this does not resolve the core issue: a substantial portion of global supply remains effectively immobilised. Estimates suggest that close to 20 million barrels per day of crude and LNG are currently stranded.

This is not merely a logistical bottleneck. It represents a significant share of global supply being withheld from the market, either through direct blockade or heightened risk aversion among shipping operators and insurers. As a result, pricing dynamics are being driven less by equilibrium and more by perceived scarcity.

We are seeing energy markets transition into a regime where prices incorporate a persistent risk premium. Even if flows begin to normalise, that premium is unlikely to disappear quickly. Forecasts pointing to a 24% aggregate increase in energy prices through 2026 reflect this reality and highlight the inflationary pressures that are now embedded in the system.

Inflation and the Policy Dilemma

The transmission of higher energy prices into broader inflation is already well underway. Energy costs feed directly into consumer prices and indirectly into nearly every sector of the economy. Transport, manufacturing, agriculture and services are all facing rising input costs, which are increasingly being passed through to consumers.

This creates a difficult environment for central banks. Traditional monetary policy tools are designed to manage demand, not supply shocks. Raising interest rates can slow consumption and investment, but it does little to increase the availability of energy.

We are therefore entering a phase that resembles stagflation. Growth is slowing, yet inflation remains elevated. For policymakers, the trade-offs are stark. Tighten too aggressively and risk a contraction in economic activity. Move too slowly and risk entrenching inflation expectations.

This tension is visible across major economies, but it is particularly relevant for countries with exposure to global energy markets. Australia, despite its resource base, is not insulated. Domestic conditions are being shaped by global price pressures and tightening financial conditions at the same time.

Australian Equity Market Under Pressure

The S&P/ASX 200 has entered May in a notably fragile position. The recent break below the 200-day moving average is not just a technical signal. It reflects a broader shift in sentiment as investors move from a position of cautious optimism to one of defensiveness.

An eight-day losing streak, the longest since 2018, highlights the speed at which positioning is being adjusted. A 6% monthly decline further underscores the scale of the reassessment taking place.

Part of the challenge lies in the structure of the index itself. Materials and financials carry significant weight, and both are sensitive to the current macro environment.

While energy stocks have benefited from higher oil prices, they are not large enough to offset declines elsewhere. The materials sector is facing a dual pressure. Higher energy costs are increasing production expenses, while concerns about global growth are weighing on demand for key commodities such as iron ore.

This combination is leading to margin compression and a reassessment of earnings expectations. Financials are navigating a similarly complex landscape. Higher interest rates may support margins in the near term, but they also raise the risk of defaults and dampen credit growth. With household budgets under strain, the resilience of the sector is being tested.

Corporate Margins and Sectoral Stress

Looking beyond the index level, the impact of elevated energy prices is being felt unevenly across sectors. Businesses with high exposure to fuel and logistics costs are among the most affected.

Retail provides a clear example. Supermarket groups are continuing to generate solid sales, yet their share prices have come under pressure. The focus has shifted from revenue growth to margin sustainability as input costs rise.

The aviation sector faces even more acute challenges. Fuel is a major component of operating costs, and the rapid increase in oil prices has forced a reassessment of profitability. Airlines have already revised fuel cost assumptions significantly higher for the second half of 2026, raising questions about capacity, pricing and demand.

What we are seeing is a shift in competitive dynamics. In a high-cost environment, companies with pricing power, operational efficiency and strong balance sheets are better positioned to navigate the pressures. Those without these attributes are likely to struggle.

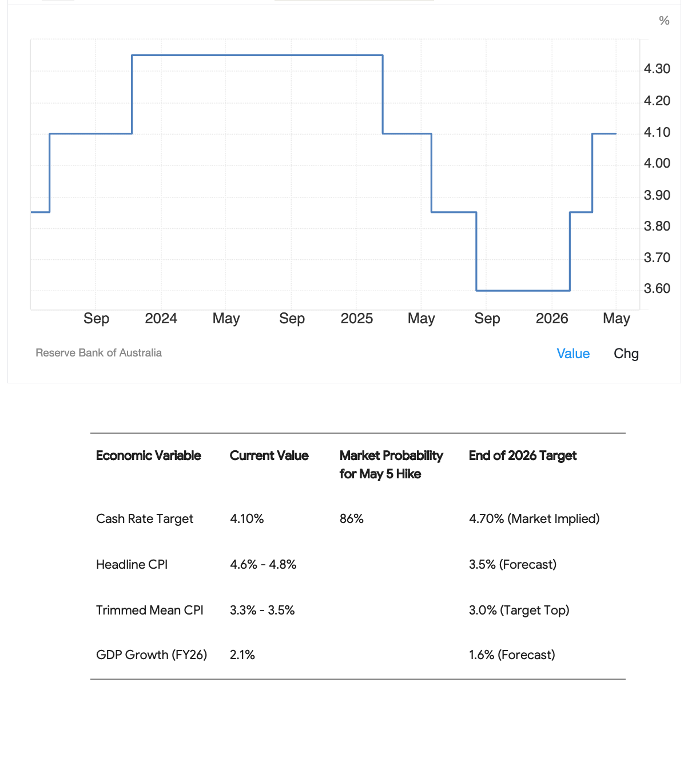

Monetary Policy in Australia

The Reserve Bank of Australia is operating within this challenging backdrop. Inflation has risen to around 4.6% in the March quarter, driven in large part by a sharp increase in petrol prices. At the same time, the labour market remains relatively tight, with unemployment near 4.25%.

Market pricing suggests a high probability of a rate hike at the May 5 meeting, with expectations for the cash rate to move to 4.35%. Beyond that, the outlook becomes more uncertain. Some projections point to a terminal rate approaching 4.85%, while others anticipate a pause as the impact of higher rates feeds through the economy.

We see the RBA facing a narrow path. The need to contain inflation is clear, but the risk of over-tightening is equally real. The combination of rising interest rates and higher living costs is already weighing on consumer sentiment, and further tightening could amplify that effect.

Source: Trading Economics, Investor Pulse Research (2026) [1]

Importantly, monetary policy cannot resolve a supply-driven shock. Even with weaker demand, constrained energy supply will continue to exert upward pressure on prices. This suggests that policy settings may remain restrictive for longer than previously expected.

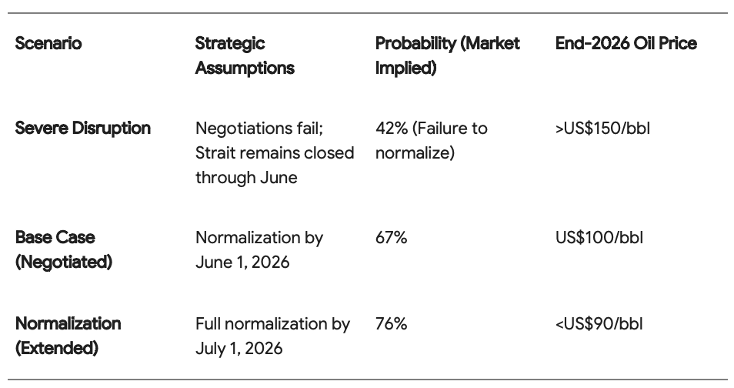

Geopolitical Scenarios and Market Implications

The trajectory of the global economy will depend heavily on how the situation in the Middle East evolves. At present, several scenarios are being considered.

Source: Energy crisis resolution modelling from prediction markets and financial institutions.

In a severe disruption scenario, where the Strait of Hormuz remains effectively closed for an extended period, oil prices could exceed US$150 per barrel. This would likely trigger a sharp slowdown in global growth and place further pressure on equity markets.

A negotiated outcome, leading to a reopening of shipping lanes by early June, represents the base case for many participants. Under this scenario, oil prices may stabilise around US$100 per barrel, providing some relief but remaining elevated.

A more constructive scenario would involve full normalisation by July, with prices falling below US$90 per barrel. This would support a recovery in sentiment and potentially allow central banks to adopt a more measured approach.

Even in the best case, however, the effects of the disruption will linger. Rebuilding inventories and restoring supply chains will take time, and the risk premium embedded in energy markets is unlikely to disappear entirely.

Strategic Responses and Global Realignment

The United States has responded with a combination of military, economic and diplomatic measures. Naval escorts are intended to restore confidence in shipping routes, while domestic policies aim to increase energy production and reduce reliance on imports.

Trade policy is also being used as a strategic tool, linking market access to energy purchasing commitments. This reflects a broader shift towards economic statecraft, where trade and energy are increasingly intertwined.

At the same time, investment in nuclear fuel independence points to a longer-term effort to diversify energy sources and support resilience. While these initiatives may reshape the energy landscape over time, they do little to alleviate immediate pressures.

Outlook for Aussie Shares

For the Australian equity market, the outlook remains closely tied to these global dynamics.

- In a bullish scenario, where the Strait reopens quickly and monetary policy stabilises, the ASX 200 could move towards the 9,200 to 9,250 range. This would likely be driven by improved sentiment and a moderation in energy prices.

- Our base case is more measured. Gradual stabilisation, combined with a pause in rate hikes after May, could see the index trade in the 8,600 to 8,800 range.

- The bearish scenario, involving prolonged disruption and further tightening, would point to a decline towards 7,300 to 7,500. This would reflect both weaker earnings and a compression in valuation multiples.

At around 17 times forward earnings, the market is still trading above its long-term average. This leaves it vulnerable to further downside if conditions deteriorate.

Investment Implications and the Case for Selectivity

In this environment, we think it is increasingly important to move away from broad, index-driven exposure and towards a more selective approach. The dispersion between winners and losers is widening, and macro conditions are amplifying those differences.

We are focusing on companies that combine strong balance sheets, resilient cash flows and the ability to maintain margins despite rising costs. These characteristics are becoming more valuable as volatility persists.

At the same time, periods of dislocation often create opportunities. High-quality businesses can become undervalued as broader sentiment turns negative, offering attractive entry points for long-term investors.

Technical positioning also matters. Stocks approaching key resistance levels, supported by solid fundamentals, may be well placed to break higher when conditions stabilise.

Against this backdrop, we have identified a group of companies that align with our current view. These are businesses that demonstrate financial strength, operate in relatively resilient sectors and, in our assessment, are trading below their intrinsic value while showing constructive technical setups.

BWP Trust (ASX: BWP)

BWP Trust maintains a unique defensive profile within the Real Estate Investment Trust (REIT) sector, primarily due to its strategic partnership with Bunnings Group. In its half-year results ending December 31, 2025, the Group reported a 3.0% increase in revenue to $103.6 million, supported by a robust portfolio occupancy of 96.7%.

The trust’s transition to an internalised management model in late 2025 has already begun to lower its cost of capital, providing a cleaner balance sheet to fund asset repurposing and growth initiatives without the drag of external management fees.

In a high-energy-price environment, BWP’s tenant mix is its primary strength. With approximately 97.6% of income secured by Wesfarmers and other national retailers, the trust is shielded from the discretionary spending volatility affecting smaller retailers.

Geopolitically, as global supply chains face localized disruptions, the "Big Box" retail format remains a critical node for domestic hardware and construction supply, ensuring steady rental growth which BWP recorded at 2.6% on a like-for-like basis in its latest report.

The rationale for BWP today lies in its capital management discipline and lease structure. With a weighted average lease expiry (WALE) of 7.5 years and a majority of leases linked to CPI or fixed percentage increases, the trust offers a natural hedge against inflation.

Its recent $300 million bond issuance in late 2025 significantly improved funding flexibility, positioning the trust to capitalize on undervalued large-format retail (LFR) assets while maintaining a capitalisation rate that reflects high-quality, land-rich underlying value.

Deterra Royalties (ASX: DRR)

Deterra Royalties operates a high-margin, low-overhead business model that is exceptionally well-suited for the current geopolitical climate. In its latest half-year accounts to December 2025, the company delivered a record Net Profit After Tax (NPAT) of $87.2 million, a 36% increase from the prior year.

This performance is underpinned by its cornerstone royalty on the Mining Area C (MAC) iron ore operations. As geopolitical tensions drive a premium for stable, Tier-1 mining jurisdictions like Western Australia, Deterra's revenue stream remains one of the most secure in the resources sector.

The company's balance sheet is a standout, ending the recent period in a net cash position of $7.2 million with zero debt. This financial strength allowed for a significant increase in the interim dividend while maintaining a disciplined payout ratio.

By divesting its non-core precious metal assets for US$82 million in early 2026, Deterra has sharpened its focus on bulk and battery metals, specifically through its investment in the Thacker Pass Lithium Project, which is critical for the energy transition and regional resource security.

The thesis for Deterra is based on "inflation-protected" earnings. Unlike traditional miners, Deterra does not face the rising energy and labour costs (OPEX) associated with extraction; it receives a percentage of revenue regardless of the operator's cost base.

As energy prices fluctuate, Deterra remains a pure play on production volumes and commodity prices, making it a highly selective, undervalued vehicle for resource exposure with a clean capital structure and significant momentum in its diversification strategy.

BlueScope Steel (ASX: BSL)

BlueScope Steel is strategically positioned as a beneficiary of "onshoring" trends and sovereign industrial capacity. Despite a challenging FY2025 where underlying EBIT was $738.2 million, the company entered 1H FY2026 with an improved outlook, forecasting EBIT in the range of $550 million to $620 million for the half.

This momentum is driven by its North American expansion and the continued dominance of its COLORBOND® brand in Australia. The latest reports highlight a successful cost-saving program, which delivered $130 million in net improvements in 2025, with a further $200 million target for 2026.

Geopolitically, the global push for infrastructure and energy-efficient building materials plays directly into BlueScope’s hands. Its robust balance sheet, featuring a mere $28 million in net debt against billions in assets, provides the resilience needed to navigate global trade shifts.

While higher electricity costs impacted recent margins, the company’s pivot toward "green steel" and electric arc furnace technology in the US positions it as a leader in industrial decarbonisation, which is increasingly prioritised by global capital flows.

We favour BlueScope as an undervalued industrial giant with substantial share price momentum potential. The company’s ongoing $240 million share buy-back program signals management's confidence in the intrinsic value of its assets.

By focusing on high-value-added coated products rather than commodity-grade steel, BlueScope maintains pricing power even as global energy prices pressure the broader manufacturing sector, making it a staple for a balanced, recovery-focused portfolio.

Bega Cheese (ASX: BGA)

Bega Cheese has successfully transitioned from a dairy commodity player to a branded food powerhouse, a move that is paying dividends in the current inflationary environment. Its FY2025 results showed a 23% increase in normalised EBITDA to $202 million, with the "Branded" segment contributing $205.2 million.

Most importantly, the company returned its "Bulk" segment to profitability, demonstrating an ability to manage the farm-gate milk price cycle effectively. This operational turnaround is key to its current undervaluation relative to its long-term earnings potential.

In terms of the balance sheet, Bega has shown significant discipline, reducing net debt by $36.3 million in the last fiscal year and bringing its leverage ratio down to a conservative 0.8 times. This financial flexibility is crucial as the company navigates the tail end of its manufacturing rationalization program.

Geopolitically, Bega is well-positioned to serve the growing "food security" demand in Asian markets, where its branded spreads and dairy products maintain high consumer trust and stable market share.

Bega makes sense today as a defensive consumer staple with growth optionality. The company has provided guidance for continued EBITDA growth in FY2026 (target $215m–$220m), supported by a pipeline of "better for you" products that cater to shifting consumer preferences.

As energy prices impact logistics and processing, Bega’s consolidation of its manufacturing footprint—such as the closure of older sites in favour of the modernised Ridge Street facility—offsets inflationary pressures and sets the stage for a breakout in profit margins.

Medibank Private (ASX: MPL)

Medibank Private continues to demonstrate the strength of a market-leading health insurer in a defensive sector. For the half-year ended December 31, 2025, Group operating profit rose 6.0% to $381.7 million, driven by resilient policyholder growth and a disciplined approach to managing claims.

Despite a broader economic slowdown, Medibank achieved a 1.9% increase in policyholders, with a notable uptick in the 25-to-30-year-old demographic, essential for the long-term health of the risk pool.

The company’s balance sheet remains exceptionally liquid, with cash and equivalents exceeding $453 million and a strong capital position that comfortably meets regulatory requirements.

While net investment income was slightly lower due to shifts in the RBA cash rate, the core insurance business maintained a stable gross margin of 16.2%. Medibank’s ability to control its expense ratio (held at 7.7%) amidst high general inflation highlights a level of operational maturity that many competitors lack.

The rationale for favouring Medibank in the current geopolitical landscape is its role as a "low-beta" stabilizer. Health insurance is a non-discretionary expense for a large portion of the Australian population, particularly as public health systems remain under pressure.

With a focus on brand differentiation and expanding its "Medibank Health" service segment, the company is not just an insurer but a healthcare provider. This vertical integration, combined with a consistent dividend policy (the interim dividend was recently set at 8.3 cents), makes it an ideal pick for investors seeking stability and reliable income.

Conclusion and Next Steps

In periods like this, the margin for error narrows. Markets are no longer rewarding indiscriminate exposure. They are rewarding precision. The combination of geopolitical uncertainty, elevated energy prices and tightening financial conditions is forcing a structural reassessment of risk across all asset classes.

This makes selectivity not just important, but essential. Every position in a portfolio needs to be justified against a more demanding set of criteria. Balance sheet strength, earnings resilience and pricing power are no longer optional qualities. They are prerequisites.

We believe this is a critical moment to reassess positioning. Portfolios built for a different macro environment may now carry unintended risks, particularly in sectors exposed to rising costs or interest rate sensitivity.

For those looking to navigate this shift with greater clarity, we are offering a Free Portfolio Review. This provides an opportunity to evaluate current holdings, identify potential vulnerabilities and explore where stronger, more resilient opportunities may exist. In a market defined by volatility and rapid change, taking a proactive approach can make a meaningful difference.

Get the wire before the market opens.

The ASX small-cap stories that matter, filed before 9am AEST. Curated by the Small Caps desk.