Winter is coming – in the northern hemisphere, that is.

And since that side of the globe hosts the largest economies, this means the world will soon need a lot of gas for heating.

Unfortunately, natural gas stockpiles have hit a 15-year low for this time of year, so it is safe to say the world is a little unprepared for the latest weather forecasts which predicted colder-than-expected temperatures, especially in the southeast and midwestern United States.

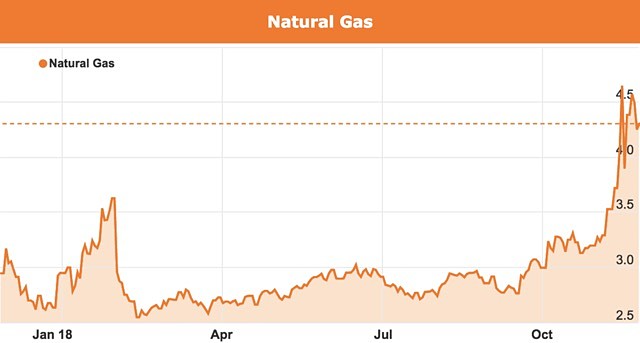

This was reflected earlier in the month when natural gas prices rocketed up to a four-year high of $4.837 per million British thermal units.

While the price has dropped slightly to its current level at $4.31, anything over $4 is still higher than it’s been since February 2014. Thus, it is important to look at what has caused this sudden spike and what may be in store for the future.

And although gas prices are rising, why is its sister commodity oil suddenly crashing?

Low inventories

Futures for December reached a peak of $4.837 per mmBtu on 14 November – the highest settlement since 26 February 2014 – although prices have eased slightly to close at $4.23 on Monday.

According to the Energy Information Administration at the time of the price hike, natural gas stockpiles in the US were standing at 3.247 trillion cubic feet – 16% below the five-year average.

When warmer weather was forecast for November a few months ago, prices stayed under $3 per mmBtu.

“The extent and breadth of [the cold snap] caught the market off guard and got prices rallying significantly,” Again Capital partner John Kilduff told reporters.

“Any kind of cold weather blast early season like this is going to cause anxiety and concerns about really tight supply as we get deeper into the winter,” he said.

US Bank senior investment strategist Rob Haworth added, “years of abundance have finally unwound in the natural gas market, with low relative inventories for this time of year now confronting cold temperatures and somewhat underwhelming seasonal bullish investor sentiment”.

The market is also entering a ‘withdrawal’ season, which typically runs from November to March, where harsh weather conditions limit production at the same time as supplies in storage are drained.

Demand rises in Asia

Demand for natural gas is expected to surge to record highs in China this winter, like it did the year before, as its ‘war on pollution’ continues and boilers and stoves using coal are increasingly replaced by units using natural gas.

In addition, India’s Prime Minister Narendra Modi last week announced that his government planned to “increase the use of natural gas by 2.5 times by the end of next decade”.

He said his administration was working towards establishing a natural gas trading exchange as part of a larger effort to relieve India’s reliance on crude oil, as well as steer the developing nation away from its worsening pollution issue.

How does this affect Australia?

While we are not facing a cold winter, our prices are certainly impacted by the larger economies in the northern hemisphere driving global prices.

Moreover, Australia has been facing future gas shortages for some time due to a number of other factors, which have also had a significant impact on price.

A major issue Australia faces is that while the country may have an abundance of gas resources, government legislation has restricted and even completely banned exploration in many regions of the country due to environmental and agricultural concerns.

Add to this, the fact that a lot of the gas that Australia is producing is being processed into LNG (liquefied natural gas) and exported out of the country.

While the Australian Energy Market Operator (AEMO) eased concerns that there will be a shortage in 2019, the problem isn’t necessarily solved but rather postponed.

In an outlook published in June, the AEMO said the crisis had been averted due to a commitment from Australia-based producers to increase domestic gas supplies following government threats to forcibly cut back on export levels.

However, the AEMO forecast that new gas infrastructure would be required from 2030 in order to continue to meet the east coast’s ongoing demand.

Dwindling production from mature fields offshore Victoria, and the fact that exploration is now banned onshore in the state, certainly don’t help ease prices.

“Gas prices have been going up on the east coast and they’re not likely to go down any time soon,” Real Energy managing director Scott Brown told Small Caps last week.

Junior gas player Real Energy (ASX: RLE) is aiming to develop its Windorah gas project in Queensland (where state legislation is more lenient on onshore gas exploration) to help alleviate the draining east coast gas market.

“There’s no new gas coming to market in [onshore Victoria and New South Wales] even though both of them would have gas under the ground that could be developed,” Mr Brown said.

“We see it as a great opportunity to supply gas at a high price,” he added.

Another vocal advocate for onshore gas exploration is former Lakes Oil (ASX: LKO) chairman Robert Annells. Speaking with Small Caps, he said there was a lot of gas onshore Victoria and prices wouldn’t be as high as they are if it was being overproduced.

“I saw a study five or six years ago – the Americans when they first started fracking and finding gas, they looked around the whole world to see where the best places were [to explore for gas]. Australia was rated number two or three in the world – but we’re not doing it,” Mr Annells said.

He added that the Victorian government’s plans to permanently ban hydraulic fracturing (the technology used to extract unconventional gas) was a bit rash, since fracking technology is changing rapidly.

“Some people have been upset about chemicals and water injected into the earth but in America they’re using other means of doing it now. So, to just ban fracking without checking the science or even allowing for it to change, I think is very short-sighted,” Mr Annells said.

He added that at current gas prices, “even a modest gas flow of let’s say half a million cubic feet per day is commercial”.

Mr Annells also pointed out that increasing supply elsewhere in Australia like Queensland or the Northern Territory, which lifted its fracking ban earlier this year, won’t necessarily alleviate gas prices. Not only is fracking a more expensive venture, there would also be extra costs associated with transportation to the east coast.

“There’s a lot of gas in the Beetaloo Basin in the Northern Territory that will require fracking and it would appear that the Northern Territory’s government is going to allow that,” he said.

“But that’s going to be expensive gas by the time you get it to market. From the Northern Territory to Sydney, or even Brisbane, is a long way. Whereas in Victoria, onshore to Melbourne, Geelong or any of the regional cities is really close.”

Oil and gas price divergence

While oil and gas are often related in terms of exploration and production, their pricing isn’t necessarily mirrored and can sometimes diverge.

This has been demonstrated in the last few weeks, with oil prices plummeting to their current level at $50.39 per barrel, a significant and steady drop over the past two months from the four-year high of $76.72 seen at the start of October.

SIA Wealth Management chief market strategist Colin Cieszynski said this divergence could be the result of some oil players turning to natural gas as a means to recover their losses.

“Natural gas is a small market… large groups of new entrants jumping on the bandwagon at once has pushed up the price,” he told reporters.

“The rally may also be taking on a life of its own, and appears to be triggering a short squeeze,” Cieszynski added.

Oil oversupply

So, while the northern hemisphere gets colder and gas stockpiles diminish earlier or greater than anticipated, leading to gas price hikes, the opposite has been the case with an overproduction of oil causing prices to fall.

According to the US Energy Information Administration, US oil production is now up at around 11.3 million barrels per day – the highest oil production on record and about 1.5MMbpd higher than a year ago.

While this production has surpassed expectations, Middle Eastern nations such as Saudi Arabia, Iraq and Iran, in addition to Russia, still account for about 80% of global supply.

These Middle Eastern countries are member nations of OPEC (the Organisation of Petroleum Exporting Countries), the international cartel that manages oil supply in an effort to set the price.

While Russia isn’t in the group, it is its biggest oil-producing ally and has backed OPEC’s plans in the past. It is little harder to sway now though, with the threat of another oil-producing non-member, the US, potentially saturating the market with its own production.

In its monthly report published in mid-November, OPEC said it expected orders for oil produced by its members to be about 31.5MMbpd – about 1.4MMbpd below current production. It also reined in its global oil demand forecast by 70,000bpd.

In an effort to offset the falling price, Saudi Arabia announced its plan to restrict output by 500,000bpd.

However, reports are that OPEC will downplay its directions to cut back on output to avoid antagonising US President Donald Trump, who’s tweet earlier in the month led to an immediate further decrease in oil prices.

Declining production in mature fields

While these actions could stabilise the price, another factor driving analysts’ forecasted recovery for the oil market is the potential for deteriorating resources to outweigh global production’s ability to keep up with demand.

According to research firm Wood Mackenzie, global production is declining in existing fields by about 5%, or 4.6MMbpd each year. Meanwhile, production based on capacity additions scheduled over the next three years are only expected to add up to 1.5MMbpd of production annually.

On the other hand, there is also the possibility that shale production could fill this gap if it continues to exceed expectations.

According to the International Energy Agency, US shale production is forecast to double from its current levels to reach 9.2MMbpd by the mid-2020s. It is also projected to account for potentially up to 75% of global production over that period of time.

If this were the case, oil prices may recover but the great ascent as seen throughout this year could well be over.