Australian shares got absolutely hammered to the tune of $50 billion-plus on Friday to record their worst week since late 2020.

It was small consolation, but the damage could have been much worse after intense stagflation fears gripped the US market, forcing the Dow Jones Industrial Average down 3.1%, the S&P 500 3.6% lower and the technology dominated Nasdaq down by a full 5%.

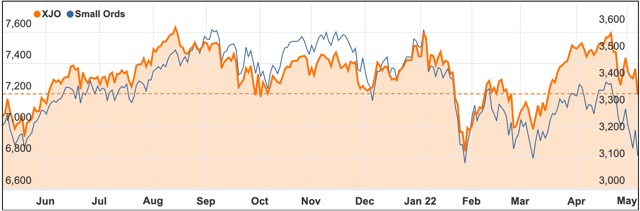

By comparison, the ASX200’s performance of losing 2.2% or 159.05 points to 7205.60 points was better than it could have been.

Bank of England’s big move spooks markets

The trigger for the market mayhem appears to be the decision by the Bank of England to raise interest rates by a full 1%, with a warning that the country should brace for double-digit inflation.

That led to a rethink of the initial market reaction to rally on the back of Wednesday’s US Fed decision to hike official rates by 0.5% to a range of 0.75 to 1%, which was initially greeted with joy by investors who were worried it might have been a rise of 0.75%.

The short-term jubilation only lasted a day before a rethink caused by the Bank of England led to a massive reversal in Thursday trade in the US as investors contemplated elevated risks of a recession both there and more generally.

All sectors hit in Australia

The damage in Australia was also unforgiving with all sectors falling although our relative lack of technology players and the presence of dominant mining and banking shares and rises in the price of iron ore and oil probably helping to limit the damage.

It was still our worst week for 18 months as technology, real estate and communication shares were hit hard.

The technology sector lost a whopping 4.5% with accounting software company Xero’s (ASX: XRO) 9% plunge a sign that the needle has swung hard away from growth and back to value.

Property stocks were hit hard as investors realised they were starting to lose their yield advantage over cash and term deposits.

Bad news for Murdoch

Rupert Murdoch’s media group News Corp (ASX: NWS) was really slammed, closing down almost 8% after falling as much as 12% after releasing a third quarter update that included plans to raise prices for its sports streaming service Kayo.

The price rise follows a 6% fall in quarterly revenue from its streaming services, with investors pondering whether subscribers hit by rising living costs and stagnant wages might just ditch their subscriptions rather than pay more for them.

Not even investment bank Macquarie Group (ASX: MQG) was spared the pain with its shares down almost 8%, despite reporting stellar earnings.

A $4.7 billion full year profit and increased dividend was not enough to hold up the share price in the face of the group warning of significantly lower income from its commodities trading arm and slowing transaction activity.

Afterpay a bright spot for Block

Interestingly, the first quarter result from Afterpay’s new owner, Jack Dorsey’s Block (ASX: SQ2), showed that the $39 billion purchase of the buy now pay later pioneer had helped the company.

Despite misgivings about BNPL companies given a souring credit picture, Block said the platform had generated US$92 million of gross profit.

That was a nice counterbalance for Block’s Bitcoin trading activities given the cryptocurrency has lost 20% in value so far this year, with trading revenues down 50% to just under US$4 billion for the quarter.

Small cap stock action

The Small Ords index dropped a whopping 5.24% to close the week on 3125.9 points.

Small cap companies making headlines this week were:

Botanix Pharmaceuticals (ASX: BOT)

Botanix Pharmaceuticals is closer to its commercialisation plans after revealing it has acquired novel dermatology asset Sofpironium Bromide gel 15% for treating primary axillary hyperhidrosis – excessive underarm sweating.

US-listed Brickell Biotech developed the gel, which has undergone phase 3 studies and a 48-week safety trial.

Botanix executive chairman Vince Ippolito said the asset would assist the company in its path to becoming a leading dermatology company.

“Having demonstrated statistically significant efficacy and favourable safety in pivotal studies, we are well-advanced in preparing Sofpironium Bromide for FDA approval in the second half of this year and look forward to accelerating Botanix into a commercial dermatology company much sooner than we originally expected,” Mr Ippolito added.

Legacy Minerals (ASX: LGM)

A partnership with Earth AI is expected to enhance Legacy Minerals’ discovery potential at its Fontenoy and Mulholland projects in New South Wales.

Earth AI has developed artificial intelligence and machine learning exploration technologies, which will be applied at Legacy’s projects.

As part of this, Earth AI will implement its artificial intelligence deposit targeting system to generate drill targets. These targets will be followed up with on-ground geophysical and geochemical exploration activities prior to any drilling.

Legacy managing director Christopher Byrne said the company’s NSW projects present significant copper-nickel-cobalt-tin and platinum group element opportunities to meet mounting demand in the battery space.

EMVision Medical Devices (ASX: EMV)

Under a new deal, NYSE-listed Keysight Technologies will exclusively supply medical technology company EMVision Medical Devices with “fast sweep” vector analysers for its neuroimaging equipment.

The agreement follows a three-year collaboration between the companies, which led to development of a personalised and miniaturised VNA solution for healthcare.

This part is a high-performance miniaturised module that enables high fidelity imaging due to its data capture speeds and measurement of cerebral blood flow with EMVision’s proprietary “pulsatility” technology.

EMVision says the exclusivity of the deal will give it a “substantial” competitive advantage and allows it to further miniaturise its imaging device.

Red Sky Energy (ASX: ROG)

Impressing investors this week was Red Sky Energy which unveiled a best estimate on the discovered petroleum initially in place for its Killanoola project of 93 million barrels of oil.

This estimate represented a whopping 1,228% increase on the previous best estimate of 7Mmbbl which was published in April last year.

Global Resources & Infrastructure (GRI) undertook the resource estimate, which includes an additional 37m of potential net pay in the Killanoola-1 DW-1 well, located in South Australia.

Red Sky has begun planning for perforation and testing of wells DW-1 and SE-1 within the project, which will be followed by extended production testing.

Altamin (ASX: AZI)

Following VBS Exchange’s unsolicited cash takeover bid, Altamin’s board announced on Wednesday that its shareholders should “take no action”.

VBS’ takeover bid valued Altamin at $37.2 million – or $0.095 a share, which was a 14% premium to Altamin’s two-month volume weighted average price of $0.085 per share.

As Altamin’s highest shareholder, VBS already owns 19.73% of the company.

Altamin has a portfolio of strategic mineral projects located in Italy, including the Gorno zinc project and the Punta Corna cobalt asset.

A scoping study published late last year gave Gorno a net present value of US$211 million based on a zinc price of US$2,850/t – well below zinc’s current levels of US$4,000/t.

Monger Gold (ASX: MMG)

Monger Gold leapt into the lithium space this week, with news it was acquiring the rights to the Scotty lithium project in southern Nevada.

Scotty comprises 700 unpatented placer mining claims covering 56sq km and is about 70km from Albemarle Corporation’s Clayton Valley (Silver Peak) development, which is the only producing lithium mine in the US.

The project also adjoins Iconic Minerals Bonnie Claire property, which has an inferred resource of 3.4Bt at 1,013ppm lithium for 18.3Mt of lithium carbonate equivalent.

Monger’s lithium news was followed up on Thursday with “further significant gold results” from diamond drilling at the Providence target within the Mt Monger North project.

Notable results were 1m at 19.19g/t gold from 99m; 8m at 4.34g/t gold from 123m, including 1m at 21.3g/t gold from 130m; and 5m at 2.11g/t gold from 108m.

The week ahead

Given the gloomy turn in world markets, the main focus for the coming week will be offshore.

Inflation data out of the US will cover rising prices on consumer, producer and trade, while Chinese international trade and inflation data will add extra details to the price rise picture.

China’s dramatic lockdowns to try to contain COVID-19 outbreaks have hit shipping and supply lines hard and kept pressure on prices – data which should also be revealed in the US numbers.

Local data, by contrast, should be fairly uneventful with figures on consumer confidence and new home sales the main feature.

Consumer confidence has been closing in on two-year lows recently and these surveys may show how consumers have reacted to rising interest and inflation rates and the continuing federal election campaign.

Overseas arrivals and departures might give us a glimpse on how tourism and immigration are recovering after lockdowns ended and a panel appearance by recently appointed Reserve Bank of Australia Deputy Governor Michele Bullock will be of interest.

Commonwealth Bank’s household spending indicator might contain some clues on how consumers are faring while figures on new home sales in April will fill out information on the troubled housing sector.

Get the wire before the market opens.

The ASX small-cap stories that matter, filed before 9am AEST. Curated by the Small Caps desk.