Weekly review: share market plunges with a strong rotation towards value

WEEKLY MARKET REPORT

The rapidly falling share market could also be telling us a story about a rotation out of high-flying technology stocks and back into value stocks.

While a $50 billion market cap drop in one day is enough news in itself, the underlying moves tell us that other factors are also at play.

Rising bond yields and inflation fears are ostensibly the reason why US markets slumped and why we followed on Friday with a 2.4% plunge in the ASX 200 to 6673.3 points – the worst fall in six months.

The underlying dynamic change, though, is that valuation is really making a comeback after a period in which it was superseded by excitement about technology and its rapidly growing global use during the COVID-19 pandemic.

Higher rates means lower share prices

Higher rates also feed through to lower profits for companies with borrowings, but the real story here seems to be that investors now have a lower tolerance for high stock prices that bear little relation to underlying profits.

The rotation was perhaps more obvious on the US market where the big technology companies that have done so much of the heavy lifting so far this year – Apple, Microsoft, Google, Netflix and Facebook – took a thumping while more value-oriented stocks did better.

In Australia everything was hit hard but still there were some signs that underlying profitability and perhaps an improved attitude to stocks that might recover from COVID-19 were treated less harshly.

Tech sector hit hardest

The worst losses were reserved for the tech sector, which sagged a collective 5.3% as buy now pay later leader Afterpay (ASX: APT) was hit hard.

After coming out of a trading halt, Afterpay shares fell 11.04% or $14.84 to $119.52 in a clear victory of experience over hope as one of the most hyped local technology stocks got a dose of reality.

A $1.5 billion convertible note offer and the news that co-chief executive officers Anthony Eisen and Nicholas Molnar have each sold 450,000 shares at $134.36 to raise a cool $60.4 million each probably didn’t help.

Afterpay wasn’t alone, with heavy drops right across all sectors including CSL (ASX: CSL) and Macquarie Group (ASX: MQG), and even the rock-solid retailers Wesfarmers (ASX: WES) and Woolworths (ASX: WOW).

Friday’s loss plunged the index into the red for the week by 1.8% and the once impressive gains for February finished at just 1%.

Profits up but shares still fall

The end of the profit season saw shares in online retailer Kogan.com (ASX: KGN) fall 10% even after net profit more than doubled to $23.6 million and revenue was up 89% to $414 million, with the interim dividend up to $0.16 a share.

Harvey Norman (ASX: HVN) also released an impressive result with net profit more than doubling to $462 million on a 25% lift in total aggregated sales of $5.1 billion, as furniture, electrical and whitegoods sales rocketed during the COVID-19 lockdowns.

Harvey Norman also boosted its dividend to $0.20 a share but its stock price was still down 1%.

There was some good news for those looking for price rises with infant formula maker Bubs (ASX: BUB) shares up 1.8% on the back of a 36% rise in goat milk formula sales to China and strong local sales.

Fund manager AMP (ASX: AMP) jumped 7.5% as it announced a partnership with US Investment firm Ares Management which will pay $1.35 billion for a 60% stake in AMP Capital’s Private Markets business.

Small cap stock action

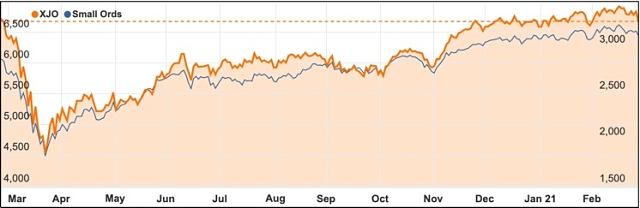

The Small Ords index fell 0.73% this week to 3123.9 points.

ASX 200 vs Small Ords

Small cap companies making headlines this week were:

Kalamazoo Resources (ASX: KZR)

Gold explorer Kalamazoo Resources has hit medium and high-grade gold below the historic Waugh pit within the Ashburton project it acquired from Northern Star Resources last year.

The company received first assays from a maiden drilling program at the project which comprised 5,718m.

Notable assays from the program were 9m at 5.52g/t gold from 148m, including 1m at 22.1g/t gold; 9m at 4.03g/t gold from 157m, including 1m at 17.8g/t gold; and 7m at 4.25g/t gold from 68m, including 3m at 7.99g/t gold from 68m.

The project currently has 1.65Moz in contained gold resources and plans to expand this beyond at least 2Moz.

Angel Seafood (ASX: AS1)

Organic oyster farmer Angel Seafood has sold 5.1 million oysters for the December 2020 half year, with the record sales up 55% on the previous corresponding period.

The sales underpinned a 52% revenue increase for the same period to $3.8 million. Driving the sales growth, and subsequent higher revenue, has been Angel’s successful penetration of Australia’s retail sector.

Angel chief executive officer Zac Halman said the result was a “fantastic outcome” for the company and he was “excited” for the future value the retail market segment will add to the company.

Lefroy Exploration (ASX: LEX)

A 10-hole drilling program at Lefroy Exploration’s Burns target, within its namesake Lefroy project, has generated “outstanding” gold and copper results.

A highlight intersection was 60m at 5.22g/t gold and 0.38% copper from 112m, including 20m at 12.2g/t gold, 0.87% copper and 1.7g/t silver.

Lefroy chairman Gordon Galt said the result was “outstanding” and the company would be following up on the intersection as soon as possible, with planning for the next phase of drilling underway.

Assays from another 10 holes completed in the same drilling program are pending.

RooLife (ASX: RLG)

After posting a strong December 2020 half year, RooLife has bedded-down its strategy to grow its presence in the Chinese online shopping market which is worth $2.2 trillion, and is 1.5 times larger than Australia’s entire gross domestic product.

The Chinese brand service industry where RooLife operates is forecast to be worth $400 billion by 2025 from its current value of $134 billion.

During the H1 2021, RooLife achieved $2.32 million in revenue, which was 44% higher than H1 FY 2020. Product sales had increased 300% to $745,000 for the period. The company anticipates $2.5 million in revenue for the March quarter alone with continued growth throughout the remainder of 2021.

Sparc Technologies (ASX: SPN)

Test work using Sparc Technologies’ graphene-enhanced adsorption material has shown it “substantially outperforms” current commercially available adsorbents.

Adsorbents are an essential part of the tailings treatment process for miners and Sparc has been developing functionalised graphene composite-based adsorbents for the removal of precious metals, oils and per- and polyfluoroalkyl substances (PFAS) contaminants.

Sparc says its material has benefits over traditional adsorbents including higher adsorption and recovery rates.

The encouraging results pave the way for Sparc to begin testing its technology at operating and residual mine sites.

Queensland Pacific Metals (ASX: QPM)

Aspiring battery chemical developer Queensland Pacific Metals has elected to more than double the capacity of its TECH Project to meet demand.

With the pre-feasibility study evaluating a plant with capacity to process 600,000 wet tonnes per annum of laterite nickel ore, the company now plans to increase this to 1.2-1.5Mtpa (wet) with production comprising key battery metals nickel and cobalt.

Queensland Pacific says the decision to grow capacity comes after discussions with potential offtake parties along with recent agreements with LG Chem and Samsung.

A definitive feasibility study will begin next month to evaluate the proposed increase.

Fatfish Group (ASX: FFG)

To further boost Fatfish Group’s majority subsidiary Smartfunding’s BNPL platform rollout throughout South East Asia, an agreement has been signed with Malaysian-based retail technology platform KryptoPOS Sdn Bhd.

The companies will work with KryptoPOS’ 5,000-plus merchants to offer the Smartfunding BNPL platform for small to medium enterprises throughout the region.

Meanwhile, earlier in the week Fatfish’s subsidiary Abelco revealed it had achieved a record $15.1 million profit for FY 2020, which was 526% higher on FY 2019.

The week ahead

With the profit season over barring a few stragglers, the highlights of the week will be the Reserve Bank Board meeting on Tuesday and the release of the National Accounts on Wednesday.

The RBA is unlikely to make any changes to Australia’s ultra-low official interest rates but the statement will be carefully watched for any signs that it might react to the higher Australian dollar and rising bond yields.

CoreLogic’s home value index for February is likely to show house prices jumped by 2% in February while the national accounts on Wednesday are expected to show the economy expanded by about 2.5%.

Overseas China’s purchasing managers indices and the US jobs numbers are the most likely releases to cause some market reaction.