Like a long-distance runner tackling a marathon for the first time, the Australian share market inched ahead again this week.

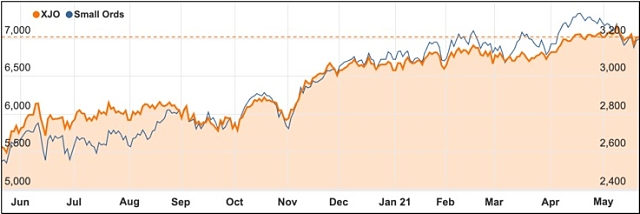

It was an agonisingly close finish with the ASX 200 up by just 10.7 points or 0.2% to 7030.3 points on Friday after various sectors jockeyed for position, with technology and healthcare helping to create the final push across the finish line.

For the week, the ASX 200 was only up a skinny 16.1 points over five sessions.

Health stocks do some heavy lifting

That impact of healthcare was shown by biotech giant CSL (ASX: CSL), which finally overcame recent weakness to add 2.2% to an impressive $284.30.

Other big healthcare names were also higher with Fisher and Paykel (ASX: FPH) up 2.8% and ResMed (ASX: RMD) adding 3.1% to play a big part in those extra 10 points.

While the rally was reasonably strong on Friday afternoon, it was uneven with the tech sector rising 1.6% even though Afterpay (ASX: APT) and Appen (ASX: APX) were lower.

EML Payments (ASX: EML) helped out with a 15.8% rise while a broad spectrum of other tech names including the controversial Nuix, Xero, Altium and Wisetech Global also gained.

Tech stronger but miners and energy stocks weaken

It was a different story for miners and energy stocks which were again weak as commodity prices continued to cool.

That included the big iron ore stocks BHP (ASX: BHP), Rio Tinto (ASX: RIO) and Fortescue Metals (ASX: FMG) which were significant drags on the wider market for the whole week after partially successful Chinese action to try to push back on rocketing iron ore prices.

Oil prices were also pulled down as Iran appeared closer to dialling back economic sanctions that have crippled its economy.

Strong economic news raises inflation fears

On the economic front, much of the news was strong, although that also fed into fears that inflation could grow some fangs and potentially slip higher, causing central banks to raise interest rates.

That was certainly the case for the Australian data which saw a better-than-expected rise in the wage price index while the unemployment rate dropped in April.

That led to speculation by traders that the Reserve Bank could see its aims of full employment and inflation within its 2-3% target zone even earlier than its own forecasts.

That is really good news but also plays into the nasty inflation narrative which is lurking in the back of traders’ minds and has also been exhibited by less conviction in the form of lower trading volumes on rising days and higher volumes on down days.

Commonwealth falls back at the $100 hurdle

In individual stock news there were a few interesting developments with banking giant Commonwealth Bank (ASX: CBA) once again falling just short of the $100 a share mark, falling $0.35 to close the week off at $98.05.

Online retailer Kogan.com (ASX: KGN) also disappointed investors with an earnings downgrade which saw its shares plummet 14.3% to $8.70.

Milk products exporter A2 Milk Company (ASX: A2M) seems to have finally turned the corner after a month of losses, finishing up 6.3% and taking its weekly rise to 0.4%.

There are a couple of trading halts to keen an eye on with shares in Airtasker (ASX: ART) halted pending a proposed equity raising and acquisition while Freedom Foods (ASX: FNP) was also put in a trading halt while the results of the company’s capital raising are tallied.

Small cap stock action

The Small Ords index rose 0.55% this week to close at 3197.5 points.

Small cap companies making headlines this week were:

QMines (ASX: QML)

ASX newcomer QMines has had early success in its maiden drilling program at the Mt Chalmers copper-gold project in Queensland.

An 11-hole diamond drilling program which totalled 1,587m was completed at the project and delivered “outstanding” results, with a 0.75m interval returning 13.4% copper, 6.11g/t gold and 31g/t silver from 132.6m.

The historic Mt Chalmers mine has been dormant for 25 years and QMines’ strategy is to bring it back online, with a further 3,000m of drilling to begin at the end of this month to validate previous data and build on the resource of 3.9Mt at 1.15% copper, 0.81g/t gold and 8.4g/t silver.

Lotus Resources (ASX: LOT)

Ore sorting test work is underway at Lotus Resources’ Kayelekera uranium project in Malawi using a 500kg sample.

This technology was not available when Kayelekera was previously in operation between 2009 and 2014 when it produced 11Mlb of uranium.

Lotus expects the technology could reduce operating costs, while boosting annual output and extending the mine life.

BPH Energy (ASX: BPH)

BPH Energy’s subsidiary Advent expects there is further potential for a gas discovery at the PEP-11 permit in the offshore Sydney Basin after a review of Geoscience Australia reports.

Advent’s additional review of the agency’s reports has confirmed a series of “large pockmarks” or distinct circular depressions that have been associated with prior gas discoveries elsewhere.

Almost 80% of wells drilled into geochemical anomalies such as these have resulted in commercial hydrocarbon discoveries, according to BHP.

Argent Minerals (ASX: ARD)

Argent Minerals has started a second round of reverse circulation drilling at its Pine Ridge tenement near its Kempfield project in central NSW.

The drilling program will comprise 20 holes for 2,390m and focus on the historic Pine Ridge underground gold mine.

Drilling aims to infill and extend historical data and follows a first pass program in 2019 which uncovered 19m at 3.2g/t gold from 98.4m, including 1m at 40.7g/t gold.

BPM Minerals (ASX: BPM)

BPM Minerals impressed investors this week with its share price rocketing more than 180% on Wednesday after it revealed it was acquiring three projects in the WA Earaheedy Basin.

The area has become a hot spot after the Rumble Resources (75%) and Zenith Resources (25%) Earaheedy joint venture discovered high-grade zinc and lead at the Chinook target.

BPM has got its hands on the Hawkins project, which is 40km northwest and along strike of the Chinook discovery.

Tietto Minerals (ASX: TIE)

West Africa-focused gold explorer Tietto Minerals has had more drilling success at its flagship 3.02Moz Abujar project in Cote d’Ivoire.

In the latest assay batch, highlight intercepts were 3m at 58.61g/t gold from 64m, including 1m at 174.72g/t gold.

These results and earlier ones, including a company best interval of 1m at 532.5g/t gold, will be used in a resource update, which is scheduled for the end of next month.

A definitive feasibility study for the project is due before the end of September.

Creso Pharma (ASX: CPH)

It was a busy week for Creso Pharma, which started with its Canadian subsidiary Mernova Medicinal Inc securing craft designation from the Ontario Cannabis Store for its Ritual Green Cannabis products.

The positive Canadian cannabis news was followed up with Creso revealing it had finalised development of its hemp flour-based Anibidoil Swine feedstock, which aims to reduce stress and support the well-being of pigs.

On Friday, Creso announced it had inked an exclusive letter of intent with Polvet Healthcare Teodorowski Spolka Jawna.

The deal paves the way for a binding agreement that would see Polvet market and distribute Creso’s animal health products in Poland, including the Anibidoil Swine feedstock.

Creso described Polvet as “an ideal partner” with an established Polish network, which has an animal health market based on 7.7 million dogs, 6.6 million cats and 11 million swine.

The deal marks Creso’s entry into the Eastern European market.

The week ahead

Once again, the strength of economic recoveries from the pandemic will be the theme for statistical releases.

Here in Australia, that will involve some reading between the lines as some of the components of the GDP numbers to be released on 2 June are gradually revealed.

Some of the things to watch out for this week include petrol prices, the used car market, consumer sentiment, April trade data, jobs and wages, discretionary and non-discretionary inflation measures, construction, mortality data, business investment and labour force estimates for April.

Overseas, the data is a bit easier to discern with the US economic growth figures on Thursday being the most obvious potential market mover.

Personal income and spending data will also feed into the inflation narrative, along with more figures on what have been some very impressive US house price increases.

Chinese industrial profits data for April is also out on Thursday.