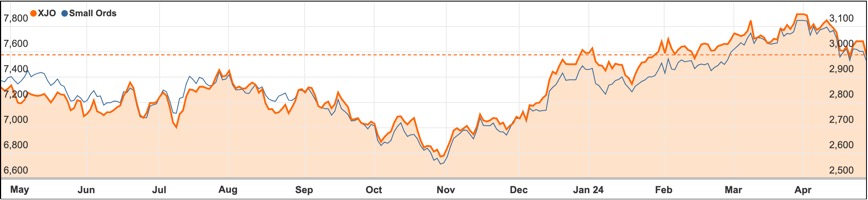

Stubbornly high Australian inflation pushed down Australian shares for the second day as hopes of interest rate cuts this year evaporated like morning mist.

Exacerbating the damage was shares in mining heavyweight BHP (ASX: BHP) which were crunched down by 4.6% to $43.15 after it finally publicly revealed a $60 billion bid for London listed miner Anglo American.

Late in the trading day Anglo American rejected the bid, labelling it “opportunistic” and claiming that it significantly undervalued the company, which includes significant copper assets.

By the end of trade on Friday, much of the gains from earlier in the week were gone with the ASX 200 down 1.4% to 7575.9 points.

That took its gain for the week to just 0.1% during a trading week that was shortened by the ANZAC Day holiday and featured rising bond yields as traders considered that the RBA might even move to raise interest rates.

Despite the downbeat general tone, there was a lot of news that pushed the share prices of individual companies in both directions on Friday.

Gold going gangbusters

One of the big beneficiaries was the gold giant Newmont Corporation (ASX: NEM) as its shares soared 13.9% to $65.70 after a memorable quarterly profit that smashed expectations due to the rallying price of gold so far this year.

There was a lot to like in the Newmont result with robust production, higher gold prices and lower operating expenses providing an ideal profit scenario.

Newmont also said there was strong interest in its sale of its non-core assets as the company continues to trim debt by reducing its workforce after the $26 billion purchase of Australian miner Newcrest in November.

ResMed shares not slumbering

Another positive reaction was the 9.6% rise in the share price of healthcare giant ResMed (ASX: RMD) to $31.50 after its net profit rose 29% to US$300.5 million (A$458 million) on sales of US$1.12 billion for the end of the March quarter.

Pending legal actions chill Super Retail shares

Less positive was the news from Rebel Sports owner Super Retail Group (ASX: SUL) which sent its shares down 3.4% to $14.37.

Pending legal action from two employees alleging a range of issues including inappropriate company travel, bullying, adverse treatment, unreasonable workload and unsatisfactory company record management will be defended by the company but will also include allegations of an alleged non-disclosure of a relationship between chief executive Anthony Heraghty and a former chief human resources officer.

Investors thought these disclosures – combined with potential claims of up to $50 million – was enough to muddy the future outlook for the owner of retail chains Supercheap Auto, BCF, Macpac, and Rebel.

Small cap stock action

The Small Ords index slipped a narrow 0.04% for the week to 2964.9 points.

Small cap companies making headlines this week were:

Base Resources (ASX: BSE)

US-based critical minerals producer Energy Fuels, has proposed to acquire Base Resources in a bid to form a billion-dollar corporation specialising in the production of rare earth elements, uranium, and mineral sands.

The offer to Base shareholders includes 0.026 Energy Fuels shares and $0.065 in cash per Base share, valuing Base at A$375 million—a 188% premium over its last closing price.

This merger will result in Base shareholders owning about 16.4% of the new entity, which will have a market capitalisation of approximately US$1.14 billion.

The acquisition aims to create a leader in the critical minerals sector, leveraging Energy Fuels’ White Mesa mill in Utah for processing monazite from Base’s Toliara project in Madagascar into rare earth oxides.

Additionally, the deal offers Base enhanced access to strategic US funding for developing the Toliara project and expanding production capacity at White Mesa.

Mayur Resources (ASX: MRL)

Mayur Resources has secured a total of $235 million in funding from Appian Capital Advisory and Vision Blue Resources to complete its Central Lime Project in Papua New Guinea.

The funding combines Appian’s definitive debt financing with Vision Blue’s proposed $63 million investment for a 49% equity stake, fully covering the project’s costs.

The construction of the project, which began in mid-2023, is expected to produce its first quicklime 18 months post-financial close, with early cash flows from unprocessed limestone sales starting in Q3 CY24.

This project marks a significant advancement for PNG, being its first industrial downstream manufacturing processing hub, which is anticipated to generate numerous jobs and contribute to the clean energy transition

The support from the PNG government underscores its commitment to enhancing the manufacturing sector and attracting significant investments to the region’s special economic zones.

Boss Energy (ASX: BOE)

Boss Energy has successfully produced the first drum of uranium at its Honeymoon project in South Australia, marking a major milestone in the commissioning process as part of the project’s restart aimed at reaching an annual production of 2.45 million pounds of uranium oxide.

The Honeymoon project, which utilises 36 million pounds out of a total resource of 71.6 million pounds, is performing above feasibility study forecasts, prompting plans to enhance production rates and extend the mine’s lifespan.

Managing director Duncan Craib highlighted the effectiveness of their mining and processing strategy, which is set to boost organic production growth and leverage existing infrastructure, alongside confirming substantial shareholder returns with the company holding $298 million in liquid assets.

In addition, Boss Energy is gearing up for the imminent start-up of the Alta Mesa uranium project in South Texas, which is expected to contribute an additional 500,000 pounds of uranium per year to Boss’ production.

This expansion aligns with the company’s strategy to enhance its international asset base, having acquired a 30% interest in Alta Mesa as part of its broader growth plans.

International Graphite (ASX: IG6)

International Graphite has received a major boost for its graphite micronising project in Western Australia with an additional $6.5 million grant from the state government, raising total state funding to $8.5 million.

The funding supports Australia’s first downstream graphite processing plant in Collie, aiming to establish a commercial-scale operation of 4,000 tonnes per annum and further develop battery anode facilities and mine-to-market strategies for the Springdale graphite project.

The project aligns with the government’s focus on green manufacturing, minerals processing, and clean energy initiatives, as evidenced by an additional $4.7 million in federal support under the Critical Minerals Development Program.

Premier Roger Cook emphasised that this initiative is pivotal for positioning Western Australia as a leader in the clean energy sector, with Collie set to play a central role in producing battery materials and offering sustainable, long-term industrial jobs as part of the region’s transition from coal.

The micronising plant will initially utilise third-party concentrate feeds, facilitating early cash flow and market establishment for its products, which are essential in lithium-ion batteries and various industrial applications.

Orion Minerals (ASX: ORN)

Orion Minerals has reported outstanding initial results from diamond drilling at the Flat Mine East prospect within its Okiep copper project in South Africa, revealing high-grade copper intercepts, including a segment of 49 meters at 4.89% copper from 231 meters depth.

This result is the highest-grade ever recorded at Flat Mines, confirming earlier findings from 1995 by Goldfields of South Africa which showed 59.1 meters at 3.55% copper.

The Okiep project covers a significant 641 square kilometres in a historically rich copper region, with over 105 million tonnes mined over the past century.

The ongoing drilling campaign, started in February, aims to confirm historical results and gather new geotechnical and metallurgical data across three target areas with a total of 5,800 meters planned.

These efforts are part of Orion’s strategy to incorporate the high-grade Flat Mine East area into its early production plans, optimising resource extraction through advanced techniques like XRF ore sorting.

The week ahead

The beginning of a new month will bring a forest of new economic data both locally and overseas.

The main data in Australia includes data on home prices, surveys of purchasing managers, retail spending, building approvals, home loans and trade.

All of that data is likely to reinforce expectations that the Australian economy is slowing as inflation stays stubbornly high, bond yield rises and expectations of interest rate cuts make way for a potentially more hawkish Reserve Bank.

Which is why the US Federal Reserve rates decision on Thursday morning our time will be closely watched with the Fed still a long way from being convinced that the rate of inflation will continue to fall to its preferred annual rate of 2%.

Interest rate outlook remains central

That means the outlook for interest rates will be the key focus for the week, along with job numbers which are expected to see a solid 246,000 jobs to be created in April.

Profit reports in the US are also expected to provide plenty of stock specific data with some of the companies reporting including Eli Lily, 3M, McDonalds, Advanced Micro Devices, Amazon, Mastercard, Pfizer, Arcelor Mittal, Moderna, Apple, Block and Janus Henderson.

Australian company trading updates include Amcor, Ampol, Coles, IGO, Liontown Resources, Macquarie Group, Megaport, Mirvac, NAB, Origin Energy, Sandfire Resources, Stockland, Syrah Resources and Woolworths.

There are also annual shareholder meetings for shareholders in Iress, Rio Tinto, TPG Telecom and Unibail-Rodamco-Westfield.

Get the wire before the market opens.

The ASX small-cap stories that matter, filed before 9am AEST. Curated by the Small Caps desk.