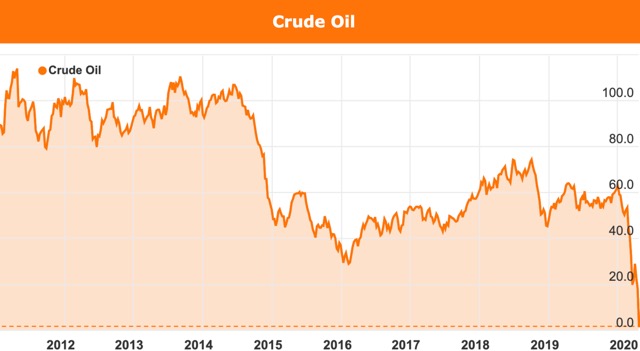

Oil price goes negative for first time in history as world runs out of storage space

A May futures contract collapsed into negative territory overnight as storage options for oil dwindle.

Wild, unprecedented, bizarre, insane — just some of the words being used in media reports to describe what happened on the oil markets overnight, when an oil futures contract went into negative territory for the first time in history.

The key to this story is that the particular May futures contract was sold overnight at -US$37.63 per barrel (-A$59.48) — yes, that is a minus sign — just one day ahead of its expiry.

That futures contract expires today (with delivery in May) for West Texas Intermediate (WTI) crude.

Clearly, the contract seller simply could not take delivery of the oil.

So, a seller was actually paying buyers to take oil off their hands because the world is running out of places to store what used to be known as ‘black gold’.

Plenty of oil but nowhere to store

Next month, some 100 million barrels of oil will be pumped around the world, with much of that having no place to go.

As one commentator expressed it, “there is so much unused oil sloshing around that American energy companies have run out of room to store it. And if there’s no place to put the oil, no one wants a crude contract that is about to come due.”

The good news: so far, this one contract is an outlier with other futures still in the green — but getting weaker.

June prices for WTI were down but still holding at around US$22/bbl.

June delivery contracts for Brent crude, the benchmark used outside the US, fell 8.9% to dip slightly below US$26/bbl.

But this begs the question: if storage cannot be found for much of May’s production, what does that portend for June’s output?

Then there is the July oil; although, by that time, the OPEC cutbacks will have relaxed a little.

OPEC cuts not enough to fix situation

The continuing oil price collapse comes just 10 days after OPEC and 10 other producing countries agreed to cut production by 9.7% from 1 May 1 for two months.

It is the biggest cutback agreement in history, but it is already looking inadequate to address the dramatic decline in consumption caused by the COVID-19 virus spreading across the world.

The cause of this latest crunch is oil storage capacity filling up, even with the agreed lower pace of production.

The oil industry is particularly watching the biggest US storage hub at Cushing, Oklahoma.

Estimates by analysts at IHS Markit indicate the world could run out of oil storage just six weeks from now — which would put pressure on OPEC and others to wind back production even further.