The Australian share market slumped badly on Friday as it reacted to a host of worrying news, including concerns that the US Federal Reserve will start raising interest rates next week.

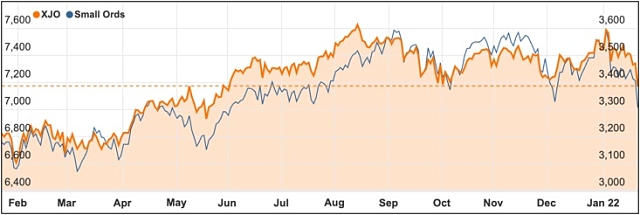

A 2.27% fall in the benchmark ASX 200 index saw 166.6 points evaporate to reach 7175.8 points, with losses very widespread across all sectors.

That brought the weekly fall to 2.95%, the biggest weekly loss in 14 months – a fall that was even greater than the US market slump which saw the Dow Jones index lose 0.95%, the S&P 500 shed 1.1% and the tech-heavy Nasdaq loses 1.3%.

Hardest hit in the market fall were the materials and energy sectors, which lost 3.52% and 3% but there were few places to hide from the falls with even defensive sectors turning negative.

Good news scarce

You had to look hard for good news but WA gold producer Ramelius Resources (ASX: RMS) put on a 2.9% rise while building materials giant Boral (ASX: BLD) shares added 2.09% and Gold Road Resources (ASX: GOR) shares were up 1.99%.

Bad news was much easier to find with the scandals coming home to roost for software provider Nuix (ASX: NXL), with shares falling a massive 22.82%.

That followed a company update that warned costly legal bills and declining revenue would impact its bottom line for the first half of the 2022 financial year.

The trading update revised its operating earnings forecast to be less than half of what it initially outlined at $13-15 million, down from $31.6 million.

BHP becomes the Big Australian again but shares drop

While an impressive 97% of BHP (ASX: BHP) shareholders approved the idea to ditch its London listing to become easily the biggest company on the ASX, the shares failed to celebrate, falling 4.8% to $45.70.

The only remaining approval required is expected from a US court later this month.

Uranium producer Paladin Energy (ASX: PDN) also had a forgettable day, with its shares shedding 10.98%.

There was also pain for buy-now-pay-later (BNPL) fintech Zip Co (ASX: Z1P) shareholders, with the stock falling by a hefty 7.76%.

Afterpay’s acquirer Block (ASX: SQ2) followed the direction of other BNPL stocks, shedding 2.34% to $172.50.

Tough times for coal and agriculture

Whitehaven Coal (ASX: WHC) shareholders also felt a 6.1% knock after the miner downgraded its FY22’s managed-run-of-mine (ROM) production by about 5% to 19-20.5Mt.

The company also reduced its managed coal sales guidance down 4% and warned of an increase of about 10% in production costs – mainly due to heavy rain, COVID-19 quarantine measures and rising diesel prices.

Shares in Australian agricultural company Nufarm (ASX: NUF) also fell 2.8% to $4.51 after announcing a debt change in its capital structure.

NUF raised US$350m in bonds – with a maturity year of 2030 – to refinance its current bond maturity profile, with the proceeds of the issue used to repay debt which matures in 2026.

Small cap stock action

The Small Ords index fell 3.10% for the week to close on 3308.5 points.

Small cap companies making headlines this week were:

Critical Resources (ASX: CRR)

After revealing it has acquired the Graphic Lake lithium project in Canada, Critical Resources confirmed the presence of high-grade lithium at its Mavis Lake project in Ontario.

Assays from resampling drill core at Mavis Lake returned up to 3.06% lithium, while rock chip samples returned a peak value of 2.39% lithium from the Pegmatite 6 prospect.

The company is awaiting permits to kick-off a maiden 5,000m drilling program at Mavis Lake.

Critical Resources managing director Alex Biggs said the company has a “high level of confidence” in Mavis Lake’s lithium potential.

Back in New South Wales, Critical Resources revealed it had intercepted visible chalcopyrite (which is associated with copper) intervals at the Gibsons prospect, which is part of the wider Halls Peak project.

Venus Metals (ASX: VMC) and Rox Resources (ASX: RXL)

In collaboration with joint venture partner Rox Resources, Venus Metals has unveiled a substantial increase to global resources at the Youanmi project to almost 3Moz.

Driving the large increase was a 156% rise in the Youanmi Deeps estimate, which now stands at 2.19Mt grading 6.89g/t gold for 2.19Moz of contained metal.

Overall, the Youanmi global resource totals 24.6Mt at 3.78g/t gold for 2.99Moz.

Rox managing director Alex Passmore said he expects the resource to be expanded further as new drill results come to hand.

“We took the decision to provide an interim updated resource estimate given the very long assay turnaround times being experienced of up to 14 weeks in some cases,” he said.

Aston Minerals (ASX: ASO)

Canada-focused explorer Aston Minerals has uncovered thick zones of nickel, while drilling the Boomerang target within its Edleston gold project.

The company intercepted 282m at 0.43% nickel and 0.014% cobalt from 186.5m, including 163.5m grading 0.52% nickel and 0.016% cobalt from 186.5m, with the final 18m of the hole returning 0.66% nickel and 0.014% cobalt from 331.7m.

According to Aston executive chairman Tolga Kumova, the scale and tenor of mineralisation hit at Boomerang is comparable to other globally significant nickel operations including BHP’s Mt Keith nickel mine near Kalgoorlie in WA.

Aston has completed drill permitting, which will allow it to drill the entire strike length of Boomerang.

Lunnon Metals (ASX: LM8)

High-grade nickel assays have continued to be generated from Lunnon Metals’ flagship Kambalda nickel project in Western Australia.

The company reported assays from the project’s Baker Shoot on Thursday where a highlight interval of 2.7m at 10.72% nickel was returned.

Other notable results were 10m at 6.82% nickel from 160m down hole; 3m at 7.88% nickel from 180m; and 2m at 4.27% nickel from 187m.

These results followed positive assays reported from the project earlier in the week, which comprised 7m at 9.22% nickel from 123m, including 6m at 10.5% nickel from 124m; and 8m at 2.52% nickel from 97m including 3m at 4.74% nickel from 102m.

Lunnon managing director Ed Ainscough said Baker was an exciting discovery for the company with more drilling to follow.

Lake Resources (ASX: LKE)

Lake Resources has doubled the proposed lithium carbonate production from its Kachi project in Argentina.

The definitive feasibility study for Kachi will now evaluate production of 50,000tpa of lithium carbonate equivalent, which is 25,000t higher than the previous proposed output.

Underpinning the expanded production is an expected increase in resources from ongoing drilling at Kachi and Lake’s other nearby projects.

Lake managing director Steve Promnitz noted the company had experienced increased demand from prospective offtake partners that are seeking environmentally-friendly generated lithium chemicals with a transparent supply chain.

He added the company has already received indicative financial support for boosting the production at Kachi from export credit agencies (ECA) in the UK and Canada, as well as support from “numerous ECA-supported banks”.

Alderan Resources (ASX: AL8)

Drilling is underway at Alderan Resources’ historic Drum mine, which has previously produced 125,000oz gold.

Mineralisation is open along strike and down dip and has not undergone any modern exploration since operations ceased in 1989.

The mine is part of the wider Detroit gold project in Utah with 10 holes planned in the current program to verify and extend known mineralisation.

Meanwhile, at Alderan’s Frisco copper project, which is also in Utah, its farm-in partner Rio Tinto subsidiarity Kennecott Exploration has firmed up three new targets.

Field inspections and surface sampling will be completed at the new targets during the current quarter and will assist with planning drill targets.

The week ahead

The main game for Australian statistical releases this week in Australia comes on Wednesday when the December quarter inflation numbers will be released – a day when markets are closed due to the Australia Day holiday.

Most analysts are tipping headline CPI to have risen by 1.1% in the quarter as higher prices for food, petrol and clothing come through.

That is likely to lift the growth in the CPI to 3.2%, although the trimmed mean CPI which the Reserve Bank monitors is likely to remain in the bank’s 2% to 3% comfort range at about 2.5%.

Other releases to watch for include consumer confidence surveys, NAB’s business survey and the producer price index.

Overseas the US Federal Reserve meeting on Tuesday and Wednesday and the inflation numbers on Thursday are the big things to watch out for.

Chinese industrial profits will also be worth keeping an eye on.

Get the wire before the market opens.

The ASX small-cap stories that matter, filed before 9am AEST. Curated by the Small Caps desk.