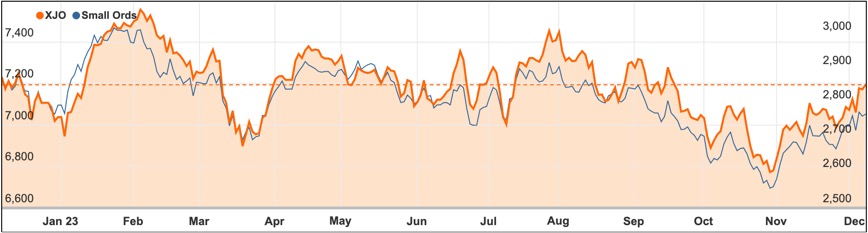

A resilient Australian share market bounced higher on Friday, shrugging off earlier losses on the back of potential takeover action and the chances that US interest rate have peaked.

By the close of trade the ASX 200 closed up 0.3% or 21.6 points higher at 7194.9 points, a 1.7% rise for the week, representing the second week of gains.

With the US market waiting for jobs data that is expected to confirm a more dovish interest rate approach from the Federal Reserve, the Australian market took a chance and rose anyway, helped out by bullish price action for iron ore.

The potential merger between Woodside and Santos sent Santos shares upwards while shares in the larger merger partner weakened.

Santos stronger while Woodside weakens

Santos (ASX: STO) shares leapt 6.2% to $7.25 despite fears of regulatory issues around the merger.

Woodside Energy (ASX: WDS) shares eased 0.5% to $29.81 as investors fear it might effectively “pay too much” for the merger.

Iron ore prices rose 1% in Singapore, which sent shares in Fortescue (ASX: FMG) up 1.1% to $25.77 while BHP (ASX: BHP) shares were up 0.7% to $47.74 and shares in Rio Tinto (ASX: RIO) were up 0.9% to $128.89.

It was a positive day for lithium explorers as well, with shares in Sayona Mining (ASX: SYA) leaping an impressive 13% to 6.1c.

More muted rises were found for Allkem (ASX: AKE), Pilbara Minerals (ASX: PLS) and Liontown Resources (ASX: LTR) which all added more than 4%.

After copping a hefty $900,000 ASIC fine for its disastrous 2015 capital raising, ANZ shares (ASX: ANZ) closed flat at $24.61.

Washington H Soul Pattinson (ASX: SOL) shares retreated 0.5% to $32.88 after it launched a $3 billion takeover bid for fund manager Perpetual (ASX: PPT), which recorded a 1.4% rise to $25.70.

Chemist Warehouse at the back door

A trading halt is continuing for Sigma Healthcare (ASX: SIG) after the announcement of a “material transaction”, which is a planned reverse listing by the much larger but unlisted Chemist Warehouse chain.

It was a strong day for the Australian dollar which rose to US66c, mainly due to weakness in the US currency as markets digested the likelihood that the Bank of Japan may move away from its ultra-low interest rate plan.

While the Aussie dollar rose, it was still down about 1% for the week after three weeks of solid gains.

The Australian market’s rise followed a 0.8% rise on Wall Street’s S&P 500 index as shares in technology stocks including Google parent Alphabet and chip maker AMD rose strongly on positive reports.

Small cap stock action

The Small Ords index rose 1.28% for the week to close at 2771.9 points.

Small cap companies making headlines this week were:

92 Energy (ASX: 92E)

92 Energy is set to merge with ATHA Energy (TSX-V: SASK) and acquire Latitude Uranium (CSE: LUR), consolidating three significant Canadian uranium explorers.

The move aims to form a leading Canada-focused uranium exploration company, with 92 Energy’s shareholders receiving an implied 78% premium on the share price prior to the announcement.

ATHA, the largest landholder in the uranium-rich Athabasca Basin, plans to raise about $25 million, making the merged entity’s cash availability around $71 million.

A key aspect of this merger is 92 Energy’s Gemini uranium discovery, which has recently revealed a parallel zone of uranium and high-grade copper mineralization, expanding the exploration potential.

92 Energy’s shareholders are advised to await further details to be provided in a scheme booklet, including an independent expert’s report and the 92 Energy board’s recommendation, expected in February 2024.

Surefire Resources (ASX: SRN)

Surefire Resources has completed a pre-feasibility study (PFS) for the Victory Bore vanadium project in Western Australia, yielding promising results.

The company plans to discuss potential collaborations with Saudi companies at a forum in Riyadh in January 2024, building on a non-binding memorandum of understanding with the Ministry of Investment Saudi Arabia for vanadium processing in Saudi Arabia.

This partnership aims to leverage the lower power and fuel costs in Saudi Arabia, reducing operating expenses and targeting nearby markets.

The Victory Bore PFS confirms a viable project, estimating annual production of 1.25 million tonnes of high-quality vanadium-titanium magnetite concentrate and up to six products, including high purity vanadium and ferrovanadium.

The project’s updated resource stands at 465 million tonnes, with plans for an optimal mining rate of 4.0 million tonnes per year, using standard open-cut methods, and shipping concentrates to Saudi Arabia for processing.

Blackstone Minerals (ASX: BSX)

Blackstone Minerals is expanding internationally by acquiring the Wabowden nickel project in Manitoba, Canada, complementing its Ta Khoa nickel refinery project in Vietnam.

The company has entered into a 12-month option agreement with CaNickel Mining, which includes staged payments totaling over $70 million in cash and shares.

This acquisition aims to secure nickel feedstock for the Ta Khoa refinery, potentially eliminating the need for third-party feedstock and aligning with Blackstone’s “green” nickel production goals, as Wabowden has access to 100% renewable power.

The acquisition fits into Blackstone’s strategy to develop a large-scale nickel mining operation, leveraging existing infrastructure and meeting the United States’ Inflation Reduction Act compliance for battery-grade nickel.

Securing a reliable, low-carbon nickel source has been a critical factor for Blackstone, especially in attracting joint venture partners for the Ta Khoa project, and this move strengthens their position in the nickel industry.

West Cobar Metals’ (ASX: WC1)

West Cobar Metals’ Salazar rare earth elements project in Western Australia has shown potential with high-grade concentrate results of 5.08% total rare earth oxides (TREO) from new metallurgy studies.

The project, one of Western Australia’s largest rare earth element explorations, has expanded its footprint to 1,171 sq km, with a significant resource estimated at 190 million tonnes at 1,172 ppm TREO.

The company is planning a drilling campaign in H1 2024 to potentially extend its Newmont prospect resource and is reviewing the extensive database of the recently acquired Dundas tenements.

Managing director Matt Szwedzicki sees the high TREO grade as a significant step towards commercialisation, noting the lower capital and operational expenditure due to the clay deposits’ nature.

West Cobar is exploring commercial pathways, including marketing the concentrate directly to downstream processors, and is also investigating co-products like titanium dioxide and alumina, with results expected in early January 2024.

Imugene (ASX: IMU)

immuno-oncology company Imugene is set to receive a European patent for its PD1-Vaxx cancer vaccine.

The vaccine, currently in clinical development for non-small cell lung cancer and colorectal cancer, is designed to activate the immune system against tumours by interfering with PD-1/PD-L1 binding.

Corresponding patent applications are pending in several countries, including Canada, China, and Australia, with grants already received in the US and Japan.

Imugene is planning phase 2 clinical trials in the UK and Australia, evaluating PD1-Vaxx in patients with operable colorectal cancer, in collaboration with the University of Southampton and The Australasian Gastro-Intestinal Trials Group.

Colorectal cancer is a major global health issue, being the third most common cancer worldwide, with over 1.2 million annual cases and a significant mortality rate.

The week ahead

There will be quite a big announcement in the coming week with the release of the Federal Government’s mid-year economic and fiscal outlook (MYEFO).

While there are plenty of Australians struggling to repay housing and other loans due to high interest rates, the Government’s Budget is expected to be in fairly robust shape so a forecast surplus would not surprise.

With the jobs market fairly strong so far despite signs that unemployment might be creeping upwards, a lot of good corporate profits and no tax cuts to pay for until the stage 3 cuts next year, the Budget position should be fairly good.

Also, Reserve Bank of Australia Governor Michele Bullock will be making a speech on Tuesday – a week before the RBA Board minutes are released for the December 5 meeting which decided to hold interest rates steady.

Consumer confidence figures are likely to show consumers are quite gloomy although the NAB (ASX: NAB) business survey is likely to find strong conditions to be holding up.

The jobs figures should continue the trend towards a gentle rise in the jobless rate.

Overseas, the main interest will be in a raft of US releases including inflation, retail sales and industrial production along with a meeting of the Federal Open Market Committee which is widely expected to hold interest rates steady.

There are also Chinese monthly releases on production, retail sales, investment and house prices.