Central banks hit quarterly record for buying gold

World Gold Council估计,各国央行在 9 月季度购买了近 400 吨黄金。

Central banks have stepped up their purchases of gold this year, according to the latest figures from the World Gold Council (WGC).

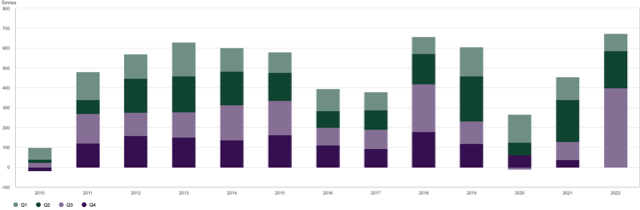

The September quarter saw the banks buy a record 399 tonnes of gold worth around US$20 billion, helping to lift global demand for the metal to 1,181t and representing a 28% increase from 922t purchased in the previous corresponding period.

A significant chunk of the demand for the year-to-date was generated during the June quarter, setting a record of nearly 400t and lifting central bank net purchases to 673t — or the highest level of any full year since 1967.

Central banks bought almost 400t of gold in Q3 of 2022.

The WGC reported that central banks added a net 59t to global gold reserves during June alone, led by Iraq which purchased 34t.

The previous month, the banks added 35t to their reserves, with Turkey (13.3t), Uzbekistan (9t), Kazakhstan (6.3t) and India (3.8t) being largely responsible for the main additions.

The total is reported to be equivalent to around one-fifth of all the gold that has ever been mined and demonstrates global appetite for the yellow metal.

Top 10 buyers

In May, global tech company Nasdaq reported that central banks in the US, Germany, Italy, France, Russia, China, Switzerland, Japan, India and the Netherlands hold the highest gold reserves (on a tonnes basis).

While there have been minor changes in positions over the years, it said the top 10 nations ranking has remained pretty much the same since 2009.

“The buying pattern by these nations and all others reflects the policy stance taken the central banks based on macroeconomic factors, financial stability and global environment,” it said.

Store of value

Gold remains a preferred store of value in case of high inflation and a safeguard against financial emergencies.

In fact, a WGC survey earlier this year found that “gold’s performance during a time of crisis and its role as a long-term store of value/inflation hedge are key determinants in the decisions of central banks to hold it”.

The metal is typically seen as a “safe asset” with a durability, scarcity and finite supply believed to provide central banks with surety and trust during times of uncertainty and market turmoil, creating “crucially stable assets” in their reserves.

Gold also tends to have an inverse relationship with the US dollar which means that central banks can load up on gold to protect the value of their reserves when the dollar loses value.

Gold-backed ETFs

On an investor level however, the WGC reported many investors sold shares in gold-backed ETFs (exchange traded funds) during the September quarter as interest rates rose and pushed up returns on other assets.

It said the offloading of bullion by ETFs helped push gold prices down 8% in the period, with the price fall helping to stimulate demand for jewellery.

This is in contrast to investor activity in May, when ETFs remained a popular play to combat rising inflation.

According to research company CFRA, gold and other precious-metals ETFs attracted 57.5% of the US$21.4 billion in positive inflows to the commodities category over the first four months of the year.