With the always useful benefit of hindsight, it is now clear that Bitcoin was perhaps the greatest speculative bubble the world has ever seen.

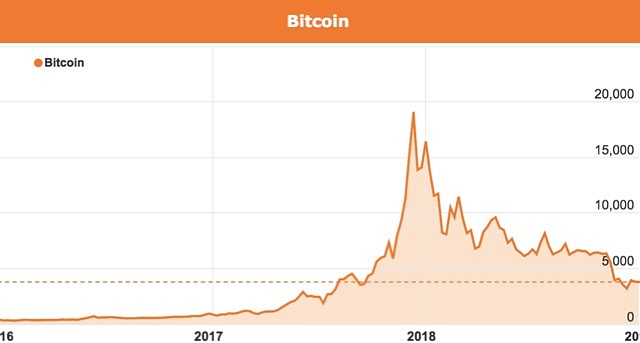

It started humbly enough with Bitcoin trading for less than US$500 before May 2016 before gently rising to less than US$2,000 by May 2017.

That was the start of a phenomenal price boom though, with the price of Bitcoin surging by almost 2,800% and reaching an incredible price peak of US$19,783 in December 2017.

It has been all downhill since then with the price plummeting all the way down to US$3,500.

Unlike similar investment bubbles such as the Dutch tulip bulb mania in the early 17th century, the Japanese property and shares boom of the 1980s and the US dotcom tech bubble, Bitcoin was the first truly global mania.

That factor alone propelled the ensuing boom much higher than those earlier ones, all of which happened when a particular set of circumstances came into play.

Mania building blocks

The basic building blocks of an investment mania are generally considered to be:

– A strong period of economic growth, which conditions investors to accept strongly rising asset prices as a “normal’’ phenomenon.

– Easily accessible credit, which can be used to buy commodities (such as tulip bulbs), physical assets (like property) or financial assets (such as stocks or bonds).

– A surprising new “asset” or technology that is seen to be capable of incredible growth in value.

Bitcoin and its many digital coin clones and “initial coin offerings’’ arrived at a perfect time to be the subject of the latest mania or investment craze.

Central banks print money

After the GFC most big central banks (notably the US, EU and Japan) had turned their money printing presses on to overdrive, slashing interest rates to incredible new lows and flooding markets with excess liquidity.

In general, the efforts of the central banks were eventually successful, breathing new life into crippled markets and slowly but surely rebuilding investor and banking confidence after the crushing frozen markets and collapsing asset values of the GFC.

Global share and bond markets gradually defrosted and asset prices across the board began to rise sustainably again.

Excess liquidity finds a home

However, all of that lovely cash had to find a home and some of it was diverted into more speculative areas, such as emerging share markets and Bitcoin.

The sexy attraction of Bitcoin is not dissimilar to earlier investment bubbles forming around the latest new technology such as railways or electricity.

Bitcoin becomes the future

Bitcoin was to be a new global currency, better than any existing currency because their scarcity value was guaranteed because they could only be produced or “mined” through the intensive use of computer time and electricity.

Unlike the irresponsible central banks that simply printed money – so the spiel went – Bitcoins were the future because they had a more secure store of value and could be transacted securely and globally with strong record-keeping using revolutionary blockchain technology.

Soon stories about people becoming millionaires through investing in Bitcoin were everywhere and the mania went into hyper-drive, as members of the general public flocked to Bitcoin to make their own fortune.

Many of these new “investors’’ were using credit to buy their Bitcoins and in some cases they were mortgaging houses and using credit cards to get a piece of the action.

Bitcoin reality is difficult

Unfortunately, despite all of the hype, Bitcoin remained a difficult beast to invest money in.

Transaction costs through competing Bitcoin exchanges are substantial and the blockchain technology in its current form proved to be quite constrained in recording transactions.

It is also quite difficult to work out the true or intrinsic value of a Bitcoin because it depends on the ability to find a “greater fool’’ to sell it to and keep the price rising rather than the cost of producing a new Bitcoin.

The fundamental value of any asset includes factors such as the ability to generate cash flow (such as interest or rental income); how scarce or rare it is (such as gold, platinum or diamonds); and its potential usefulness (such as coal, iron ore or lithium).

Property is a sort of combination asset because it can have value due to the scarcity of land in a particular area and also has the ability to generate a rental income.

Bitcoin doesn’t really have much in the way of intrinsic value or usefulness in earning an income.

That didn’t stop it becoming part of a “euphoric’’ price boom, in which true value is lost and investors simply look at the rising price as proof that their investment is working.

So why did Bitcoin crash?

The one thing that happens to all bubbles is that something comes along to finally deflate them.

Usually quickly and brutally for assets with limited liquidity, such as Bitcoin, but occasionally in a bruising but slower fall for assets with greater liquidity, such as stocks.

Once a speculative asset stops rising in price, those who own it through heavy borrowings quickly realise that the interest cost of holding on can no longer be paid for by capital gains.

Once they decide to start selling, the price begins to fall faster and the familiar rush to the exits leads to even more precipitous price falls, such as those that Bitcoin has suffered.

Also, in the case of Bitcoin concerns about increased government regulation of crypto-assets played a big part in the decline, along with the possible introduction of central bank digital currencies.

A large number of scandals in which Bitcoins went missing or were stolen and the collapse of some crypto exchanges didn’t help matters.

Investment mania is not new

While Bitcoin is a modern invention, there is nothing new about investment bubbles which have been around virtually forever.

In his noted book Extraordinary Popular Delusions and the Madness of Crowds, Scottish poet, journalist, author, anthologist, novelist and songwriter Charles Mackay talked about how whole communities could “fix their minds upon one object and go mad in its pursuit”.

Then, many people “become simultaneously impressed with one delusion, and run after it, till their attention is caught by some new folly more captivating than the first”.

That book was written way back in 1841 and looks largely at the Dutch tulip mania among others but as Bitcoin shows us, there is nothing new under the sun.

The only difference now is that an investment bubble can be global, which seems to make its rise and demise all the greater.

Get the wire before the market opens.

The ASX small-cap stories that matter, filed before 9am AEST. Curated by the Small Caps desk.