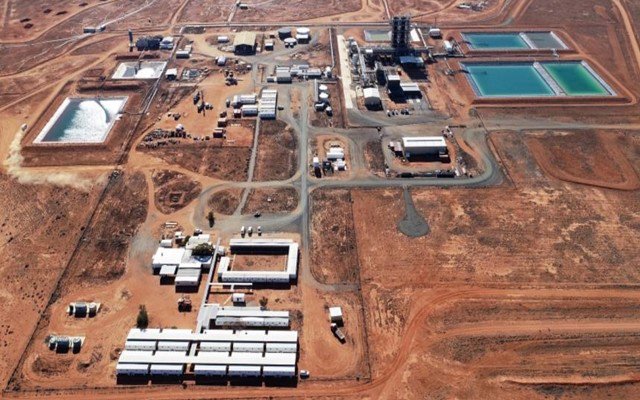

Boss Energy (ASX: BOE) has unveiled its much anticipated enhanced feasibility study for the proposed Honeymoon uranium mine in South Australia, with the study identifying lower costs and a higher pre-tax net present value of US$309 million (A$411.93 million).

The US$309 million NPV is 35% more than estimated in last year’s feasibility study.

In the enhanced study, the forecast pre-tax IRR is 47%, while the earnings before interest tax depreciation and amortisation margin is estimated at 62%.

Post-tax free cash flow is up from US$332 million to U$425 million, with gross life of mine revenue of almost US$1.28 billion calculated.

Underpinning this is a 22.5% increase to nameplate production capacity to 2.45 million pounds of uranium.

Total payback has decreased from four to 3.5 years.

“The study shows conclusively that the changes we plan to make to the processing plant will increase annual product, cut costs significantly and increase overall financial returns,” Boss managing director Duncan Craib said.

Cost savings

Part of the study’s intent was to pinpoint ways to decrease expenditure to ensure Honeymoon became one of the lowest cost uranium mines globally.

As a result, all-in costs have fallen 11% to US$31.86 per pound of uranium produced, with all-in-sustaining costs reduced by 16% to US$25.62/lb, and cash costs estimated to be 21% lower at US$18.46/lb.

A 14% decrease to the restart capital cost was identified, with this figure sliding from US$69.68 million to US$60.19 million.

All-up the capital cost which has the additional IX columns totals US$80.01 million, including contingencies.

Boss describes this as an industry competitive up-front capital requirement.

Better outlook

As well as revising capital and operating estimates, the enhanced feasibility study takes into account the improved outlook for the uranium sector.

“With forecast all-in costs of US$31.86/lb and contract uranium prices running in the high US$30s/lb, Honeymoon is already poised to be an extremely robust project,” Mr Craib said.

“The outlook is even stronger when viewed against the widely-held belief in financial and energy markets that the uranium price is set to continue climbing on the back of a supply shortage, declining inventories and growing demand due to its carbon free status.”

Mr Craib added the company was “perfectly placed” to capitalise on the strengthening uranium market with its existing plane, mine and tier one location with predicted low costs and strong financial returns.

Near-term plans

Boss plans to advance exploration at Honeymoon to grow the resource and mine life, with many “highly promising” near mine and regional targets identified.

Additionally, to get the project into production, Boss is progressing offtake negotiations and financing efforts.

The company has also purchased 1.25Mlb of uranium on the spot market, which will de-risk the mine through re-start and commissioning.

Boss expects to leverage off any future appreciation of the uranium price with the inventory.