- 01Oil jumps on US-Iran tensions; Hormuz risk rises.

- 02Hormuz disruption = higher supply risk; insurers pull cover.

- 03Mining rally seen as awareness phase; long cycles persist.

Energy markets set the tone for the broader geopolitical backdrop as crude oil moved sharply higher into the weekend. Traders had already begun pricing in elevated risk after US-Iran negotiations in Geneva over Iran’s nuclear program concluded without tangible progress toward a deal.

President Trump signalled that Iran was not negotiating in good faith, while the United States, China and several other nations advised their citizens to leave parts of the region, an unmistakable indication that escalation risk was rising.

Those warnings proved prescient. Over the weekend, the US and Israel launched coordinated strikes on Iran, prompting retaliatory missile activity targeting neighbouring countries that host US military assets.

Although Iranian officials stated that the Strait of Hormuz remains open, reported attacks on oil tankers have significantly elevated supply risk. The Strait is one of the most strategically critical chokepoints in global energy markets, with approximately 20% of global oil supply transiting this narrow waterway. Even limited disruption carries meaningful consequences for pricing, shipping logistics, insurance costs and physical supply flows.

The response from the shipping industry was immediate. Insurers reportedly withdrew coverage for vessels entering the region, a decisive step that effectively constrains trade even if the waterway is technically open. This is a key transmission mechanism: geopolitical tension quickly becomes a physical supply constraint.

In parallel, OPEC signalled plans to resume production increases in April, amounting to approximately 206,000 barrels per day. However, incremental supply additions may prove insufficient if transit through Hormuz remains impaired or materially disrupted.

The collapse of diplomatic talks and the escalation into maritime risk represent the most consequential scenario for global energy markets. It underscores a broader reality central to our positioning: geopolitical fragmentation and supply vulnerability are no longer theoretical risks. They are active forces driving repricing across the commodity complex and energy is often the first signal.

That signal now feeds directly into metals.

The surge in metal prices has renewed speculation about a mining peak, a view that fails to reflect the industry’s structural realities. Two strong years do not reverse decades of neglect. In our view, what we have witnessed is a wake-up call, not a market top.

Mining is defined by long development timelines, rigid supply growth and capital cycles that unfold over decades, not quarters. The forces underpinning today’s repricing, prolonged underinvestment, constrained supply and rising structural demand, remain intact and unresolved.

What we are seeing is the awareness phase of a bull market. Institutions were caught off guard and rushed to deploy capital without sufficient industry expertise, pushing prices higher across the sector.

At the core of the mining industry lies the metal price cycle. And at the centre of that cycle stands gold. Gold sets the tone. Understanding its behaviour is essential to understanding what ultimately unfolds across the broader metals complex.

In our view, we are at the beginning of one of the largest rotations out of financial assets and into hard assets in modern history. Comparing the size of the gold market to global equities cuts through narrative and highlights just how early this rebalancing remains relative to traditional financial assets.

Neither the macro regime nor industry fundamentals suggest late-cycle conditions.

Viewed through this lens, recent price moves in hard assets are not signs of excess. They represent the opening phase of a much larger repricing.

The structural forces driving this shift are self-reinforcing:

- Record sovereign debt driven by persistent twin deficits

- A constrained Federal Reserve limited by the rising cost of debt service

- A global financial system reliant on inflation to reduce leverage

- Accelerating central bank gold accumulation to restore monetary credibility

- Constrained supply of gold and critical metals after decades of underinvestment

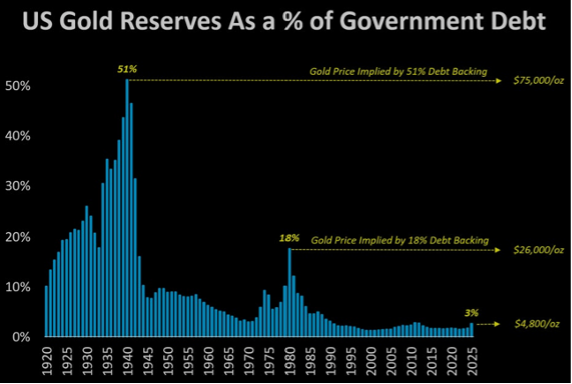

Focusing on the US alone provides useful historical context. During the last period of extreme debt expansion during World War II the US government debt surged to levels comparable to today. At that time, roughly 51% of federal debt was backed by gold reserves.

Today, total debt is materially larger, yet only around 3% is backed by gold. The contrast is stark and illustrates how deeply undervalued gold appears when measured against sovereign balance sheets.

Without speculation, we look at the math.

If US government debt were backed by gold at the same 51% ratio observed in the 1940s, total US gold reserves would need to be valued at roughly $20 trillion. With 261.5 million ounces of gold, that equates to a price approaching $75,000 per ounce.

While unrealistic and unlikely, the number sets a conversation for painting what the upper limit might look like given historical trends. It reflects historical precedent applied to present-day balance sheet realities. The divergence between sovereign liabilities and the monetary anchor that once supported them is wider today than at any point in modern financial history.

With that backdrop established, we turn to what we view as the largest dislocation in markets today: mining equities.

For decades, the mining industry endured poor capital discipline, limited exploration success, stagnant production growth and near-total abandonment by institutional investors. Talent exited the sector. New projects were not advanced. Mining ceased to be viewed as an attractive long-term career.

What distinguishes this period is that mining is not being displaced or disrupted, it is being rediscovered as essential. The global economy is relearning that metals form the foundation of everything we are attempting to build next.

Deglobalisation, supply-chain decoupling and resource nationalism all point in the same direction. So too does the enormous requirement for reliable electricity to power AI infrastructure, data centres, automation and industrial reshoring. Layer on record government debt and financial repression, and the direction becomes increasingly evident.

All roads lead to metals.

From a demand perspective, this does not resemble the final stage of a mining cycle. In our view, it represents the first meaningful step forward after years of stagnation.

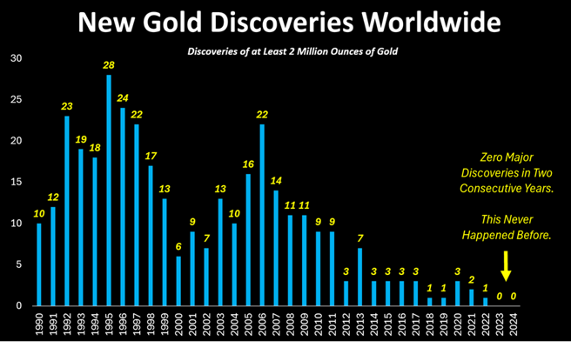

The supply challenge reinforces this conclusion. For the first time in recorded history, global data indicate zero gold discoveries across two consecutive years. This has never occurred before. And the issue is not confined to gold.

Major discoveries across most metals have fallen into the single digits, with few projects in the development pipeline capable of materially shifting the global supply curve.

The same narrative once used to dismiss senior gold miners is now being applied to silver equities. Underperformance is again being labelled “structural.” History suggests that framing may once again prove incorrect.

The valuation disconnect is significant.

Silver mining equities are trading at historically depressed levels relative to the metal itself. Even under optimistic assumptions - meaningful new discoveries and sustained production growth - current valuations remain difficult to justify, in our view.

For us, this is not a short-term trade. Our process centres on identifying structural mispricing’s and positioning ahead of the curve rather than reacting to near-term price volatility.

Mining remains in a secular bull market in our assessment. Volatility is not a flaw in that thesis; it is the mechanism through which capital-intensive industries reprice.

Most primary silver producers continue to operate with all-in sustaining costs well below $20 per ounce. Yet equity valuations implicitly assume silver prices will revert toward those cost levels.

That assumption requires a macroeconomic, monetary and supply backdrop that we believe is largely behind us for the coming decade.

Few industries span the full arc of human economic development.

Mining does.

Long before modern markets, governments or currencies, the extraction of stone and metal enabled humanity’s earliest technological progress.

What we are witnessing today is not the end of a cycle, but the re-emergence of one of the world’s most essential industries. This is the reawakening of mining, metals, geoscience and the material foundation of the global economy.

Let the cycle continue.

Mining equities remain profoundly undervalued relative to underlying metal prices and relative to the traditional financial assets that dominate institutional portfolios.

Persistent misunderstanding of the industry, combined with a shortage of capital allocators possessing genuine mining expertise, has created a compelling opportunity within this specialised segment of capital markets.

For over a decade, we have successfully managed Growth, Income and Balanced portfolios for self-funded retirees and time-poor professionals. To learn more about our HIN-Direct wealth management services, please contact me at mark.elzayed@investorpulse.com.au

Get the wire before the market opens.

The ASX small-cap stories that matter, filed before 9am AEST. Curated by the Small Caps desk.