- 01Cost-up world: energy, freight, labour, insurance rise.

- 02Sydney 95 ULP shortages signal tighter supply.

- 03Oil: multi-year supply deficit; demand steady.

Firstly, a thanks to the North Sydney Sun bears for having me aboard this season and a valiant fight in the Grand Final on Saturday. We were unable to pick up the win but preseason starts today and we look forward to next season.

Now on with it and it’s not looking amazing…

Little interview with a very impressive CEO late last week. Check out my chat with Kerrie Matthews from Locksley Resources (ASX: LKY).

Everything is getting more expensive. Not in the economist-on-TV sense, but in the lived, daily, “why is this suddenly twenty bucks?” sense.

We’ve entered a structural cost-up world, and the receipts are finally screaming loud enough that people are noticing. Energy, food, freight, labour, insurance—pick a category and it’s either constrained, disrupted, or structurally under‑invested.

Bowser Yowser

And now we’re seeing the pointy end of it: Sydney service stations literally running out of 95 ULP. Not “tight supply,” not “higher prices,” but empty bowsers.

This is what the early innings of a cost-up world look like. Shortages first; prices second; political excuses third.

I try and steer clear of encouraging a direction and merely commentate from the back of the bus, but if the RBA hikes now it’s not only unnecessary and callous but also cruel.

The increase in basic necessities has already led to the cutting back of much else for Australian families, and that’s if you can actually find what you need to purchase.

The RBA needs to hold until there is some certainty of what’s ahead.

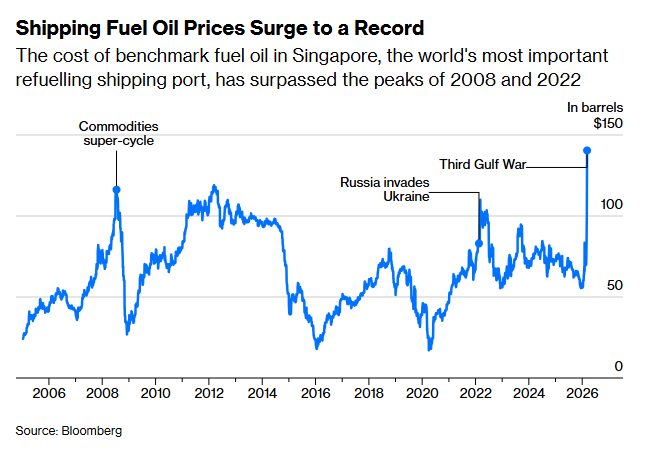

It’s all about shipping fuel. It’s the stuff that comes out the bottom of the refining process and it’s only good for container, oil and bulk shipping. The price of this has gone crazy. So while the usual oil price we see is still below record highs, the actual, relevant cost of shilling oil has gone bananas.

Oil: The spark waiting for a match

If you want the clearest articulation of where this goes, look at the latest commentary from Jeff Currie at Carlyle Energy Pathways (ex GS Strategy and someone I absolutely listen to).

His call is blunt: we’re in a multi‑year structural supply deficit. A decade of under‑investment, declining OPEC+ spare capacity, and US shale no longer acting as the world’s swing producer have created a setup where supply simply cannot meet steady demand.

He pushes back hard on the “peak demand” narrative. Jet fuel is rising, petrochemicals are rebounding, India is the new marginal consumer, and China’s slowdown is overstated.

As he puts it: “Demand doesn’t need to boom-it just needs to stay steady while supply falls. That’s how you get violent repricing.”

Layer on top a market that is catastrophically mispricing geopolitical risk—Hormuz, the Red Sea, Iran, shipping insurance—and you have the makings of an oil market that could move to $150–$200; much faster than consensus thinks.

And the kicker: the US Strategic Petroleum Reserve is still partially depleted. The buffer is gone.

Here is the summary on a Bloomberg Interview the other day which pretty much follows my reasoning. Even if peace were declared today, we’re already past the point of no return.

Refining: The bottleneck no-one talks about

Jack Prandelli’s refining explainer cuts straight to the heart of what’s going on.

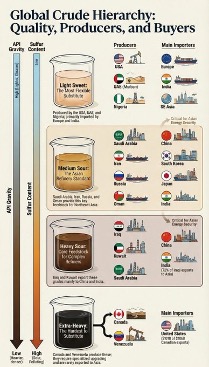

Crude oil isn’t one “thing”, and refineries aren’t interchangeable. Different refineries are built for different grades of crude, and Australia imports most of its refined fuel. When global crude flows shift—sanctions, war, shipping delays—the refineries that can process the available crude get overloaded, and the ones that can’t sit idle.

The bottleneck isn’t crude. It’s refining capacity.

High‑octane fuels like 95 and 98 ULP require more complex cracking, higher‑quality feedstock, and more energy per litre. When refineries are stretched, premium fuels disappear first.

Add shipping disruptions—longer routes, fewer tankers, higher freight costs—and Australia, sitting at the end of the supply chain, gets hit hardest.

As Prandelli puts it: “We don’t have a crude problem. We have a refining problem. And refining problems show up as empty bowsers.”

Tech: The Iran War’s hidden casualty

Morgan Stanley’s Shawn Kim made a point this week that should have rattled the entire tech sector: the Iran conflict isn’t just a geopolitical story-it’s a direct threat to global semiconductor production.

AI and advanced chips may be the cutting edge, but they run on something far more basic: energy. And a huge share of that energy flows through the Strait of Hormuz.

Taiwan, home to the world’s leading‑edge chip production, runs fabs so power‑hungry that “one major manufacturer alone accounts for roughly 9–10% of the country’s total electricity consumption.”

Taiwan relies heavily on imported LNG, but only holds 1.5 weeks of inventory, with a few more weeks on ships. If Hormuz is disrupted, those ships don’t arrive. If they don’t arrive, fabs don’t run. And if fabs don’t run, the global AI build‑out stalls.

Kim’s warning is simple: the war turns a Middle‑East conflict into a global tech bottleneck.

Similar to commodities, see the crocodile mouth open up with the rising line being the price of the commodity and the declining line being the companies that can’t actually sell it. Similar in the industrial and precious metals space too in my humble view.

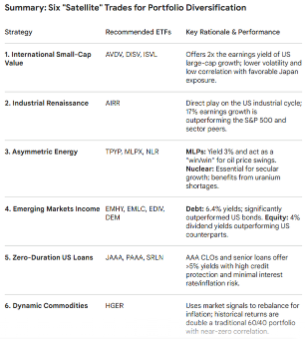

Six Satellite Trades for Diversification

To close, here’s the diversification table-six satellite trades that sit outside the usual 60/40 thinking courtesy of BofA:

PS: The thing no-one is looking at

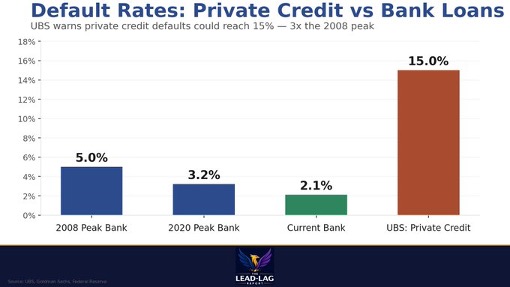

While the world is glued to the war ticker, there’s a monster hiding in plain sight: the private‑credit time bomb.

UBS is warning of potential 15% default rates-triple the 2008 bank‑loan peak.

In any other week, this would dominate the headlines. In any other week, the media would also still be chewing on the Epstein fallout.

This would be three times the rate of the peak of bank loan defaults in 2008.

But war has a way of swallowing every other story. And right now, it’s the only thing big enough to bury both a credit crisis and a scandal that refuses to die.

Stay safe and all the best,

James

Get the wire before the market opens.

The ASX small-cap stories that matter, filed before 9am AEST. Curated by the Small Caps desk.