- 01US bull 3.5y, +99%, likely to persist.

- 02Fuel crisis fuels inflation.

- 03Food crisis: 363m at hunger risk.

- 04Small caps under the radar.

Theory of Thing Investment Podcast: We finished last week with a deep dive into the ongoing fuel crisis, which continues to rattle global supply chains and household budgets alike.

While the headlines are dominated by these energy shocks, the US market is busy rewriting the record books yet again.

In our latest podcast episode, we break down these record highs and spotlight a few small cap companies that are currently flying under the radar but demand your attention.

Listen or watch the full breakdown via the links.

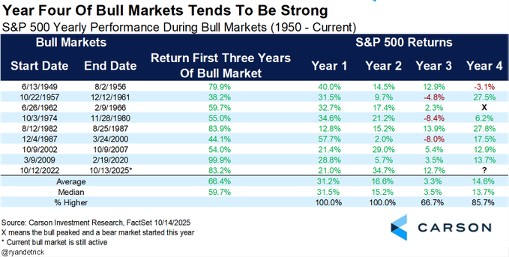

The 3.5 Year Itch: Why this bull has legs

To the US market: The current bull market is now 3.5 years old and has surged an impressive 99.2%.

While some investors are starting to look for the exit, history suggests that once a bull market celebrates its third birthday, it rarely ends in the near term.

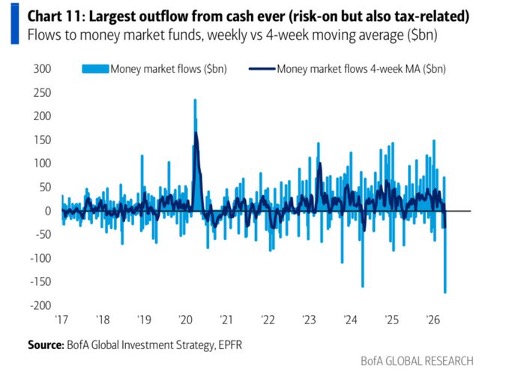

Looking back over the last 50 years, five bull markets made it past the three year mark and lasted an average of eight years. We are seeing capital actively chasing this momentum, evidenced by the largest outflows from money market funds on record.

The wall of worry is being climbed by a massive wave of liquidity.

The ‘I Told You So’ Moment: The global food crisis

I have been talking about the impending food crisis for a long time now, and the rest of the world is finally starting to catch up to the reality of the situation. A major report just published in the Financial Times (18 April, 2026) confirms that we are staring down a systemic catastrophe.

The crux of the issue is the "Hormuz to harvest" transmission. Because our modern food production is so tightly linked to fossil fuel inputs, the conflict in the Middle East isn't just a fuel problem; it's a fertilizer and famine problem. The report highlights that hunger and even famine are now foreseeable consequences of the war on Iran.

The World Food Programme is currently warning that 363 million people are at risk of acute hunger this year. This isn't a future threat. It is a slow moving disaster where farmers are planting less today because they can't afford inputs, leading to smaller harvests and even higher prices in the second half of the year. Wealthier nations will see this as inflation, but for the world's poorest, it is a matter of survival.

We have discussed the strategic importance of agricultural positioning before, and this data confirms that the supply side of the global pantry is under extreme duress. When you combine energy shortages with fertilizer scarcity, you get a compounding effect that most models haven't fully priced in yet.

Local Reality: Markets v the economy

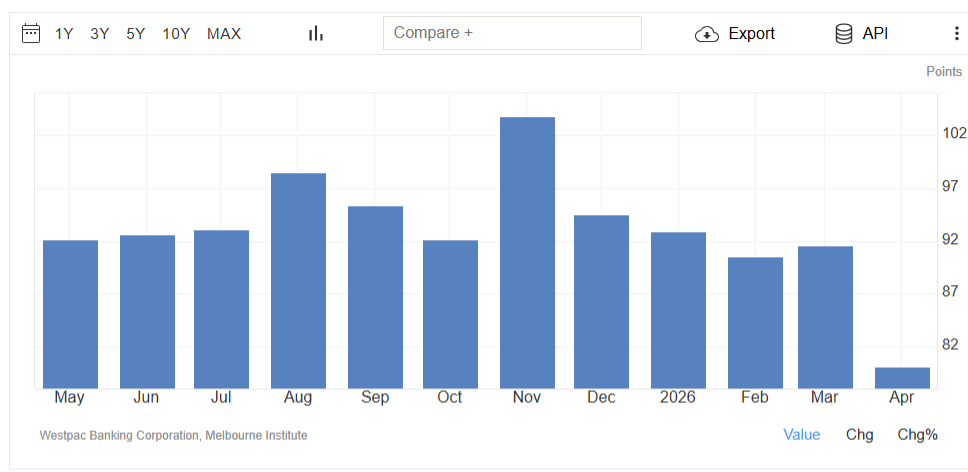

It is vital to remember that US markets are not Australian markets, and more importantly, markets are definitely not the economy. While Wall Street celebrates, the local sentiment tells a far more sobering story.

Australia’s Westpac–Melbourne Institute Consumer Sentiment Index plunged 12.5% from a month earlier to 80.1 in April 2026, marking the biggest monthly decline since the onset of the COVID pandemic and hitting its lowest level since November 2023.

Despite this collapse in sentiment, the RBA is still widely expected to deliver a 25bps hike on 5 May, a move already priced in by bond markets and major bank analysts. However, I still believe a surprise hold and a "wait and see" approach is in order and significantly underpriced.

The disconnect is jarring. We have banks predicting further hikes while simultaneously whispering about recessionary risks. It is a two headed beast tearing itself apart.

My view remains controversial: after this hold, the next move will be down. We are seeing the limits of consumer resilience in real time, and further tightening into a 12.5% sentiment drop feels like a policy error in the making.

The Global Liquidity Shift

We often talk about where the "smart money" is going, but right now, it’s about where the "scared money" is leaving.

Those record outflows from money market funds I mentioned earlier aren't just moving into blue chips. They are moving into a market that is fundamentally disconnected from the underlying economic pain being felt by the average consumer.

For high net worth investors, this creates a unique environment where momentum is the primary driver, but the structural foundations (food, energy, local sentiment) are showing deep cracks.

Stay diversified, look at the hard assets, and keep an eye on those small caps that can weather a local downturn. The market is giving us a gift in terms of momentum, but the economy is giving us a warning.

Conspiracy of the Week

We close with a look at the more eccentric corners of the internet.

The latest theory circulating suggests that the US had been operating a network of radars designed to control the weather over Iran, effectively holding back the clouds.

The "proof" being offered? Now that these systems have allegedly been knocked out, the rain has finally started to fall. You can track the chatter and see the claims for yourself here.

It’s a wild thought to end on, but in a world where global supply chains and local economies feel increasingly chaotic, sometimes a weather-controlling radar is the simplest story people can find.

Stay safe and all the best.

Get the wire before the market opens.

The ASX small-cap stories that matter, filed before 9am AEST. Curated by the Small Caps desk.