- 01Grow your own food; hedge against shocks.

- 02Fertiliser/energy costs imply higher food inflation.

- 03RBA cuts likely when something breaks; markets lag.

I spent the weekend doing what every calm, rational market observer apparently does when confidence is high and systems feel stretched. I was repotting chilli seedlings.

Each plant was carefully moved into its own container, soil refreshed, roots teased out, and labels rewritten. This was not just a gardening exercise. It was preparation for a world that is starting to look less resilient than advertised.

Diesel constraints, fragile logistics, geopolitical stress, and an increasingly brittle global supply system all argue for redundancy. That includes food.

Man cannot live on chilli alone, so the rest of the weekend was spent preparing beds for broccoli, spinach, carrots, and whatever else might thrive if imported abundance proves less reliable. Leafy greens beat leverage. Root vegetables beat narratives. Grow your own food while you still can.

This may sound like tin foil hat behavior. I prefer to think of it as diversification away from just in time everything.

That mindset also informed a call I made publicly on Twitter. I said that the next move by the Reserve Bank of Australia would not be up. It would be down.

The backlash was immediate and surprisingly hostile. Inflation is still too high, I was told. Central banks cannot blink. This cycle is different. Rates must stay restrictive.

The reaction itself was the signal. A large segment of people are still anchored to backward looking data and are mistaking recent prints for current conditions. The market itself is not yet reflecting the same view, but markets are reactive, not prophetic. They wait for confirmation, then they reprice quickly and pretend it was obvious all along.

Central banks do not cut because inflation hits target. They cut because something breaks. The fact that this idea still provokes anger tells you how far there is to go before consensus catches up with reality.

If you’re going to be over-allocated then the bond market looks the place to do it. However, the timing of this is tricky, since inflation will keep rising (and yields too more or less) before the back breaks and everything has to be cut, stimulus, money printing etc.

Food—Always Thinking with Your Stomach

One place reality is already visible is food.

Look at the Green Markets weekly North America fertiliser price index. The chart shows unmistakable stress.

Fertiliser prices surged violently in 2022, reaching the highest levels since the GFC. They came off, but they never returned to the previous regime. They are now sitting at a structurally higher plateau.

Fertiliser is energy intensive, diesel heavy, and globally traded. When fertiliser prices remain elevated, food prices follow with a lag. This is not something monetary policy models well. It also does not show up cleanly in consumer price indices until it is socially and politically uncomfortable.

Food inflation does not need to accelerate for pressure to build. It only needs to stay high while income growth slows and credit tightens.

Fuel and Some Ideas

Diesel is another area where stress is already visible if you bother to look.

A friend of mine Tom built https://checkpetrol.com.au. It maps fuel availability across Australia, showing where servos are out and where they are not.

Here's a link to his feed.

He deserves all the credit. I’d trust this over anything the government wants to put out for a while.

Funnily enough on the radar today is Janus Electric Holdings (ASX: JNS) we’ve followed them for a while and they’ve had a bit of a day today.

Simple (he says) idea of fleet trucks with replaceable batteries. I’ve liked the name and there could be a little more value there, if you think a trucking industry keen to get off a diesel dependence.

$20m cap, yeah it’s probably got a few legs on it from here.

Scroll through regional areas and patterns emerge. Outages are not everywhere. They do not need to be. Stress in fuel systems appears at the edges first. Diesel, in particular, fails in pockets, then corridors, then regions.

Diesel is the bloodstream of the real economy. Farming, fertiliser production, freight, and food distribution all depend on it. When availability becomes patchy, costs rise quietly and reliability falls quietly. The data lags. The consequences do not.

The Clock Is Ticking

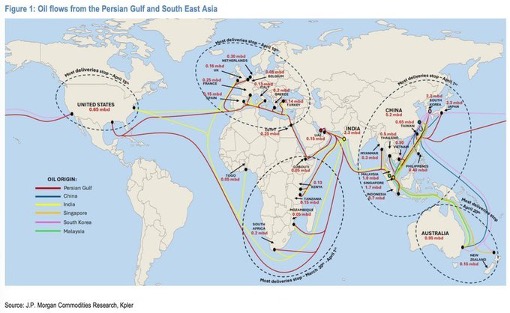

J.P. Morgan recently circulated a chart mapping global oil flows and, more importantly, where deliveries stop when those flows are disrupted. Australia sits at the far end of those routes. When things work, distance does not matter. When they do not, geography suddenly reasserts itself.

Oil does not disappear evenly. Cargoes are redirected. Insurance costs spike. Long routes are sacrificed first. This is not a theory. It is logistics.

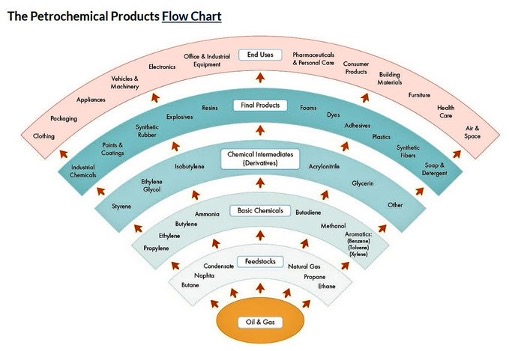

At this point it is also worth clearing up a persistent misconception. Oil is not just energy. It is everything else.

The petrochemical products flow chart makes this explicit. Oil and gas feed into chemical feedstocks. Those feed basic chemicals. From there come intermediates, resins, fibres, solvents, foams, and plastics.

At the top of the chain are finished goods that feel mundane until they are missing. Packaging, clothing, appliances, vehicles, electronics, medical equipment, pharmaceuticals, fertilisers, and building materials.

This is why supply disruptions are not linear. You do not just get higher petrol prices. You get friction everywhere. Substitutions, shortages, quality downgrades, and delays that never quite get captured cleanly in inflation statistics.

Which brings us to a final, telling datapoint.

Plastic—It’s Everywhere

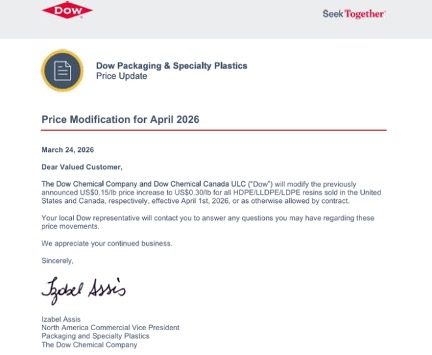

Dow Chemical has just doubled its planned price increase on resin. Not doubling the price. Doubling the increase. The previously announced US 0.15 dollars per pound rise has been revised to US 0.30 dollars per pound on key polyethylene resins, effective April.

Resin sits squarely in the middle of the petrochemical flow chart. It is downstream of oil and gas and upstream of almost everything physical. Packaging, medical supplies, consumer goods, construction materials, electronics casings, and food wrapping all rely on it.

When resin costs rise, manufacturers absorb what they can. Margins compress. Specifications are adjusted. Price lists move slowly. But when increases are revised higher before implementation, it tells you that input costs are rising faster than expected and supply reliability is under strain.

This is how inflation reenters the system after everyone declares victory. Not through wages or coffee prices, but through industrial inputs that touch everything quietly.

Put all of this together. Fertiliser prices that refuse to normalise. Patchy diesel availability. Oil flows that prioritise core routes over distant ones. Rising resin costs at the heart of the petrochemical stack.

This is not a call for panic (well…actually). It is a plumbing inspection.

When pipes strain, pressure changes well before the lights go out. Central banks respond to outcomes, not early warnings. That is why they always appear late.

Which brings us back, inevitably, to the garden.

If the world muddles through, I will have a surplus of chillies. If it does not, I will still have a surplus of chillies. Either way, the logic holds.

Grow your own food while you still can.

Stay safe and all the best.

PS: Boots on the ground this week if you follow the indicators. Also, the cut to the fuel excise will only make it cheaper for people to hoard petrol.

Get the wire before the market opens.

The ASX small-cap stories that matter, filed before 9am AEST. Curated by the Small Caps desk.