- 01Copper/silver demand intact; focus on cash-flow.

- 02AIS down ~32% YTD; H1 PAT $47.9m, EBITDA $133m.

- 03Top peers show cash-flow moat; SFR, DVP, A1M, HGO, CYM.

The recent weakness in Aeris Resources (ASX: AIS) is not just a story about one stock losing momentum. It is a window into how quickly markets are shifting their focus.

On one hand, the long-term case for copper and silver remains compelling, driven by electrification, grid expansion and sustained industrial demand. On the other, the way investors are choosing to access that opportunity is changing just as fast.

We are now seeing a clear divide emerge. Capital is no longer flowing indiscriminately into the sector. Instead, it is concentrating in names where the link between investment and cash flow is clearer and more immediate.

That helps explain the relative strength we are observing in peers such as Sandfire Resources (ASX: SFR), Develop Global (ASX: DVP), AIC Mines (ASX: A1M), Hillgrove Resources (ASX: HGO), and Cyprium Metals (ASX: CYM).

In this environment, simply being exposed to the right commodity is no longer enough. Copper and silver may offer structural upside, but the dispersion in outcomes between companies is widening. That makes stock selection more important than ever.

We continue to be highly selective, focusing on businesses with defensible moats, strong balance sheets and consistent cash flow generation, a discipline that is reflected in our portfolio performance.

==Only available to our Small Caps readers, I am offering a Free Portfolio Review. Click here to send me a copy of your portfolio in excel format and take a closer look at how your portfolio is currently positioned.==

Aeris Resources a Compelling Opportunity

Since the start of 2026, AIS has fallen from a peak near $0.70 to around $0.36 to $0.40, a decline of roughly 31.55% year to date. This comes after a one year return exceeding 105%, making the reversal striking.

Looking at the trading pattern, we see clear signs of distribution. March was decisive, with a 10.47% drop on March 23 followed by another 7.06% decline within days. Even when Aeris price action attempted to stabilise, the recovery failed to hold.

This is not simply a case of weak sentiment. It reflects a market deliberately repricing the risk.

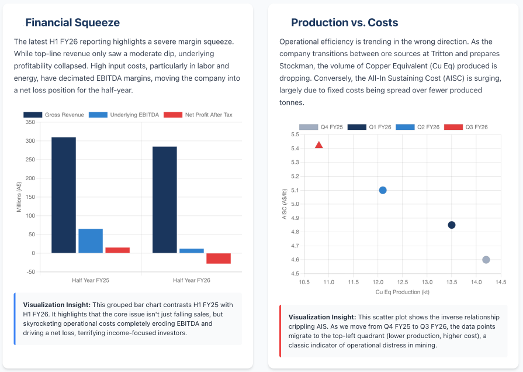

On the fundamental side, the company has delivered. For the half year to December 2025, net profit after tax came in at $47.9m, up 62% year on year. That alone exceeds the entire FY25 profit of $45.2m.

Revenue rose 5% to $306.3m, but more importantly, cost discipline drove margin expansion. Cost of sales fell 9%, lifting gross profit by 57% to $93.5m. EBITDA followed, rising 57% to $133m, while operating cash flow increased 67% to $97.3m.

Earnings per share reached 4.7 cents, which on paper places the stock at an attractive valuation relative to peers.

Yet we are not seeing that reflected in price. The market is clearly discounting something else.

Balance Sheet Strength with A Caveat

We also note that AIS has achieved a key milestone by moving to a debt free position. Following a $96.9m equity raise, the company repaid its $50m facility, removing roughly $6m in annual interest costs.

Cash and receivables now exceed $106m. That provides flexibility, at least in theory.

However, the market is not rewarding this. The reason is straightforward. Investors are focusing less on what sits on the balance sheet today, and more on how quickly it may be deployed.

A Shift in Narrative from Producer to Builder

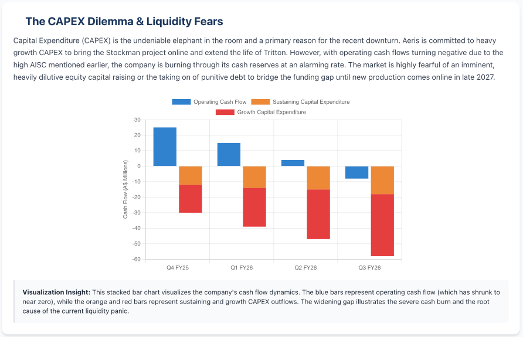

The acquisition of Peel Mining, valued at approximately $214m, marks a turning point. Strategically, it makes sense. It consolidates assets, expands the copper resource base beyond 500,000 tonnes, and extends the potential life of the Tritton operation to more than a decade.

But the structure matters. Peel shareholders will own about 20.5% of the combined entity. That level of dilution changes the investment equation immediately.

At the same time, the story shifts. We move from a company generating cash today to one investing heavily for tomorrow. Markets tend to assign lower multiples to that transition, particularly when timelines stretch and execution risk increases.

The CapEx Reality We Have to Factor in

Capital expenditure is central to this re-rating. Quarterly capex is running at around $40m to $41m, with a large share directed toward development.

Murrawombie alone accounted for roughly $23m in pre-strip and cutback work. Tritton continues to absorb capital through infrastructure upgrades, including plant improvements and maintenance.

Looking ahead, Constellation will require significant additional investment as it moves into construction. At the same time, bonding requirements are locking up cash that cannot be redeployed elsewhere.

When we put this together, the picture becomes clearer. Cash outflows are immediate and visible. Returns are further out and still dependent on execution.

Short-Term Friction Amplifies the Pressure

We also need to account for operational disruptions. The rail bridge issue has resulted in around 5,000 tonnes of concentrate sitting on site, equivalent to roughly $18m in delayed revenue.

While this is ultimately a timing issue, it affects how the market perceives cash flow. In the current environment, perception matters.

Operationally, Tritton delivered 11,141 tonnes of copper in the half-year, up from 8,832 tonnes previously. However, quarter on quarter performance was affected by a 10 day shutdown and lower grades from development ore.

Cracow produced 11,100 ounces in the quarter, but with an all in sustaining cost near A$3,278 per ounce, margins remain tight despite strong gold prices.

What we see is progress, but not without friction. That inconsistency is enough to unsettle investors.

Market Becoming More Selective

When we step back, the re rating of AIS fits into a broader pattern. Capital is rotating toward clarity. Investors are favouring businesses where the link between capital invested and cash flow generated is more immediate and easier to assess.

That helps explain the interest in names such as Sandfire Resources, which offers scale and diversified production, and Develop Global, where execution discipline has been a defining feature.

We are also seeing attention on more focused plays like AIC Mines, as well as emerging producers such as Hillgrove Resources.

Further along the risk curve, Cyprium Metals is attracting interest where project optionality aligns with a supportive copper price environment.

Bigger Picture Remains Intact

Importantly, the broader thematic backdrop has not changed. Copper remains central to electrification, grid expansion and energy transition. Supply constraints continue to build, while demand is structurally supported.

Silver is also gaining relevance through its role in solar and industrial applications, adding another layer of support across the complex.

From that perspective, the current divergence between companies is less about the metals themselves and more about how each business is positioned to capture that demand.

For AIS, the path forward is clear. The company has demonstrated profitability and strengthened its balance sheet. The next step is execution.

We will be watching for the ramp-up at Murrawombie, the release of the $18m in stockpiled concentrate, and clearer visibility on how Constellation is funded and delivered.

Until those pieces fall into place, it is understandable that the market applies a discount.

Where We See Opportunity Emerging

This brings us to the more constructive question. If capital is rotating, where is it going, and why?

As AIS navigates its transition, we are seeing a growing focus on opportunities where the risk-reward balance is more immediate, where dilution is limited, and where the pathway from resource to cash flow is clearer.

Let’s take a closer look at five solid buy opportunities across the copper and silver space, including Sandfire Resources, Develop Global, AIC Mines, Hillgrove Resources, and Cyprium Metals, and outline why they may offer a more direct route to capturing the structural upside in the sector.

Sandfire Resources

We see Sandfire as the heavyweight in this group, having successfully moved past its old DeGrussa days to become a true global producer. By focusing on the MATSA operations in Spain and the Motive project in Botswana, they’ve planted themselves in stable, high-quality jurisdictions.

In our view, Sandfire is the perfect high-beta play for this environment; because they own modern processing hubs, they aren't as vulnerable to the smelting bottlenecks that are currently hurting smaller explorers. They are essentially positioned to ride the wave of decarbonization demand that we expect will keep supply tight for the rest of the decade.

When we dive into the numbers from the FY2025 results and the March 2026 Quarterly, the scale is impressive. They’ve pulled in $1.17 billion (USD) in annual revenue and turned a solid $90 million (USD) net profit.

What really catches our eye, though, is the 7.73% free cash flow yield. It’s rare to find a copper pure play that generates this much cash while still growing. With a Price/Free Cash Flow ratio of 12.93 and a recent interim dividend of $0.03, we think they offer a great balance of returning capital to us as shareholders while keeping enough in the tank for expansion.

For our portfolio, Sandfire acts as a stabilized cornerstone. With a market cap of about $8.12 billion, they have the balance sheet strength to weather any short-term macro wobbles. Their April 8, 2026, update confirmed they are hitting their production targets and moving into higher-grade zones at MATSA, which should help keep unit costs down.

In a world where copper concentrate is getting harder to find, we believe owning a company with a proven, internal supply chain like Sandfire is a very smart move.

Develop Global

We really like the dual threat model Develop has built. They aren't just mining copper at their flagship Woodlawn project; they also run a specialized underground mining services arm. This gives us a "picks and shovels" revenue stream that keeps ticking over even when commodity prices get jumpy.

As of our latest check in April 26, Woodlawn has hit steady state production. This is a huge milestone because it officially moves them from being a "story" stock to a producer at a time when copper prices are near record highs.

Looking at the June 2025 financials, we can see the growth engine is humming. Revenue jumped to $231.47 million (AUD), up from $147.22 million the year before. More importantly, they flipped a net loss into a $72.39 million (AUD) profit.

We’re seeing an EPS of $0.224 and a P/E ratio of 24.80, which tells us the market is starting to recognize the long term value here. For us, the 6.02% free cash flow yield is the standout figure, especially since they are still aggressively developing the Kiana and Sulphide targets.

We think Develop is a unique addition to a portfolio because they own the talent. There is a massive global shortage of underground mining expertise, and by having that team in-house, Develop can expand their own mines cheaper and faster than their peers.

With a market cap of $1.83 billion, we see plenty of room for growth as they continue to prove they can deliver complex projects that others might struggle with.

AIC Mines

AIC Mines is a classic "hub and spoke" success story in our eyes. Their strategy revolves around the Eloise Copper Mine in Queensland, where they are integrating the nearby Jericho deposit into their existing processing plant.

We think this makes total sense in today’s inflationary world, instead of spending hundreds of millions on a new plant, they are just plugging new ore into an old one. This keeps their capital costs down and allows them to increase production volumes without the usual headache of massive debt.

The numbers from the March 2026 Quarterly back this up beautifully. We’re looking at $189.55 million (AUD) in revenue and a net profit of $14.95 million (AUD). What really stands out to us is the 15.34% free cash flow yield. That is a massive number for a company of this size.

With a Price/Free Cash Flow ratio of only 6.51, we feel the market is currently undervaluing how much cash this business is generating.

From a portfolio perspective, we see AIC as a value plus growth pick. They have a P/E ratio of 17.18, but because their earnings are growing so fast, their PEG ratio is a tiny 0.02. That’s a signal to us that the market hasn't fully priced in the production jump coming from Jericho.

They’ve also recently bumped up their Ore Reserves, which gives us more confidence in the mine's longevity. For those of us looking for high-margin copper exposure without the mid-tier price tag, AIC is a very compelling case.

Hillgrove Resources

We see Hillgrove as a company that has finally reached its inflection point. They’ve spent a lot of time and money getting the Kanmantoo Underground mine ready, and now we are finally seeing the payoff.

They have a massive processing plant that’s been under-utilised for years, and now that they have two mining fronts open, including the Nugent development, they are aiming to push through 1.7–1.8 Mtpa by the middle of this year. We love this setup because the infrastructure is already paid for; every extra tonne they mine now is mostly pure profit.

If we look at the FY2025 report from February, revenue hit $167.6 million (AUD), which is a big leap from $112.2 million. Even though the bottom-line net profit looked small at $0.1 million, we aren't worried. That figure includes a lot of non-cash depreciation and a heavy $40.3 million reinvestment into the mine.

The real story for us is the $26.0 million EBITDA and the $35.8 million in operating cash flow. They have navigated the risky development phase and are now entering the "harvest" phase.

We think the rationale for holding Hillgrove is the valuation gap. They are trading at a Price/Sales multiple of just 1x, which is quite low compared to their peers. Analysts are looking for 72.2% annual earnings growth as they tap into the high-grade Emily Star zones.

For our portfolio, Hillgrove represents a turnaround play that is backed by real, physical infrastructure in a safe place like South Australia. It’s a high-leverage way to play the copper price.

Cyprium Metals

Cyprium is the "wildcard" in our list, and we treat it differently than the others. They are working on restarting the Nifty Copper Project using a heap leach process to create copper cathode.

We find this strategy very attractive right now because heap leaching uses less energy and less upfront cash than a traditional smelter. In a market where smelting capacity is tight, being able to produce a finished copper product right at the mine site is a huge advantage.

Since they are in a restart phase, the financials are exactly what we’d expect: zero revenue and a $17.0 million (AUD) loss in the latest annual report.

But we aren't looking at current earnings here; we are looking at the assets. They just raised $5.03 million to finish their technical studies, and they are sitting on a massive mineral resource. At today’s copper price of $12,100/t, that resource is worth significantly more than the company’s current market value.

For us, Cyprium is an optionality play. Trading at a Price/Book ratio of 1.18, so we are basically buying the assets at cost and getting the upside for free if they successfully restart the mine.

It’s the highest risk stock on our list, but if they hit their production targets, the move from "developer" to "producer" usually triggers an immediate re rate. We see it as a great speculative satellite holding to complement the steadier cash flow machines like Sandfire.

The key takeaway is that the copper and silver thematic remains firmly intact, but the market is becoming far more selective in how it rewards exposure to that theme. Investors are no longer simply paying for resource size or commodity leverage. They are looking for balance sheet strength, disciplined capital allocation, near-term cash flow and clear execution pathways.

Against that backdrop, we believe the opportunity set is shifting toward companies that can either generate cash today or provide a more direct line of sight to production growth.

Sandfire offers scale and global copper exposure. Develop Global combines production with mining services capability. AIC Mines provides a strong hub-and-spoke growth profile. Hillgrove offers operational leverage through existing infrastructure. Cyprium remains the higher-risk optionality play, but one with meaningful upside if Nifty is successfully restarted.

Get the wire before the market opens.

The ASX small-cap stories that matter, filed before 9am AEST. Curated by the Small Caps desk.